Regions Bank 2013 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2013 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20

|

|

10 REGIONS 2013 YEAR IN REVIEW

Even as we work to create deeper relationships with existing

customers, we also are committed to developing new

relationships as well. In 2013, our associates found new

ways to serve more consumers more effectively. A standout

was indirect auto loans, which grew by 32 percent. That

progress was the result of growth in our collaboration

with dealers — now numbering more than 2,100 — and

technology that accelerates loan processing for dealers

and their car buyers. Our consumer credit card offering

also proved attractive in the marketplace. The number of

active Regions card users increased 7 percent over the

prior year. These successes — and others — helped us

grow the total number of customers and households

served across the company in 2013.

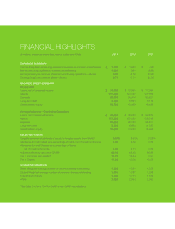

Positive Financial and Operational Performance

Strong execution and effective expense management by

our team contributed to positive financial results in 2013.

Net income available to common shareholders increased

10 percent from the prior year to $1.09 billion. Diluted

earnings per common share grew more than 8 percent, to

$0.77 per share. Net interest margin expanded by 9 basis

points, to 3.20 percent at year-end. Positive trends in our

deposit mix resulted in a 15 basis point decline in deposit

costs to a historically low level of 15 basis points in 2013.

While we restored growth in loans and households in

2013, we kept a sharp focus on controlling expenses

and driving greater efficiency across the organization.

Each year since 2009 we have consistently reduced

full-year adjusted expenses*, and we extended that

strong record in 2013, while we also made appropriate

investments in new customer-facing, revenue-generating

positions and took necessary steps to strengthen our

compliance organization.

Asset quality is another vital measure of our financial health.

In 2013 we achieved broad-based improvement in every

metric, including a 31 percent decline in net charge-offs

and a 36 percent decline in total nonperforming loans.

As we work to continue driving loan growth going forward,

we are guided by a mandate that risk management is

a fundamental requirement throughout each of our

17 businesses. Our training and internal communication

make clear that it is a responsibility shared by every

associate everywhere we do business.

Regions’ capital position also remains strong as our Tier 1

common ratio* was 11.2 percent, an increase of 40 basis

points from one year ago. The company’s liquidity position

remained solid as we concluded 2013 with a loan-to-deposit

ratio of 81 percent.

Driving Innovation with a Personal Touch

We are focused on offering customers flexible options that

allow them to bank how they want, when they want, in

whatever manner they find most convenient. Technological

innovation is transforming the delivery of financial services,

adding both efficiency and convenience. In 2013, we

continued to enhance our digital solutions, including our

remote capture deposit product for mobile banking cus-

tomers. The growth in our mobile banking channel has

been nothing short of extraordinary, and in the not-too-

distant future we expect mobile transaction volumes to

surpass that of the Internet channel.

As we invest to expand our digital capabilities, we remain

firm in our belief that banking remains, at its core, a people-

based business. It is clear that our 1,705 branches remain

a source of Regions’ strength and provide a competitive

advantage in the marketplace. Eighty-one percent of

our sales originate in the branch and 64 percent of our

11.2%

10.8%

8.5%2011

2012

2013

Tier 1

Common

Ratio*

270 bps

Increase

0.15%

0.30%

0.49%2011

2012

2013

Deposit

Costs

34 bps

Improvement

*See Table 2 in Form 10-K for GAAP to non-GAAP reconciliations.