Baskin Robbins 2015 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2015 Baskin Robbins annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

-47-

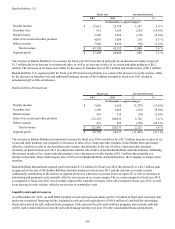

undrawn at closing. As of December 26, 2015, there was approximately $2.48 billion of total principal outstanding on the Class

A-2 Notes, while there was $73.7 million in available commitments under the Variable Funding Notes as $26.3 million of

letters of credit were outstanding.

On January 26, 2015, DB Master Finance LLC (the “Master Issuer”), a limited-purpose, bankruptcy-remote, wholly-owned

indirect subsidiary of Dunkin’ Brands Group, Inc. (“DBGI”), entered into a base indenture and a related supplemental indenture

(collectively, the “Indenture”) under which the Master Issuer may issue multiple series of notes. On the same date, the Master

Issuer issued Series 2015-1 3.262% Fixed Rate Senior Secured Notes, Class A-2-I (the “Class A-2-I Notes”) with an initial

principal amount of $750.0 million and Series 2015-1 3.980% Fixed Rate Senior Secured Notes, Class A-2-II (the “Class A-2-II

Notes” and, together with the Class A-2-I Notes, the “Class A-2 Notes”) with an initial principal amount of $1.75 billion. In

addition, the Master Issuer also issued Series 2015-1 Variable Funding Senior Secured Notes, Class A-1 (the “Variable Funding

Notes” and, together with the Class A-2 Notes, the “Notes”), which allows the Master Issuer to borrow up to $100.0 million on

a revolving basis. The Variable Funding Notes may also be used to issue letters of credit. The Notes were issued in a

securitization transaction pursuant to which most of the Company’s domestic and certain of its foreign revenue-generating

assets, consisting principally of franchise-related agreements, real estate assets, and intellectual property and license

agreements for the use of intellectual property, are held by the Master Issuer and certain other limited-purpose, bankruptcy-

remote, wholly-owned indirect subsidiaries of the Company that act as guarantors of the Notes and that have pledged

substantially all of their assets to secure the Notes.

The legal final maturity date of the Class A-2 Notes is in February 2045, but it is anticipated that, unless earlier prepaid to the

extent permitted under the Indenture, the Class A-2-I Notes will be repaid in February 2019 and the Class A-2-II Notes will be

repaid in February 2022 (the “Anticipated Repayment Dates”). Principal amortization repayments, payable quarterly, are

required on the Class A-2-I Notes and Class A-2-II Notes equal to $7.5 million and $17.5 million, respectively, per calendar

year through the respective Anticipated Repayment Dates. No principal payments will be required if a specified leverage ratio,

which is a measure of outstanding debt to earnings before interest, taxes, depreciation, and amortization, adjusted for certain

items (as specified in the Indenture), is less than or equal to 5.0 to 1.0. If the Class A-2 Notes have not been repaid in full by

their respective Anticipated Repayment Dates, a rapid amortization event will occur in which residual net cash flows of the

Master Issuer, after making certain required payments, will be applied to the outstanding principal of the Class A-2 Notes.

Various other events, including failure to maintain a minimum ratio of net cash flows to debt service, may also cause a rapid

amortization event.

It is anticipated that the principal and interest on the Variable Funding Notes will be repaid in full on or prior to February 2020,

subject to two additional one-year extensions.

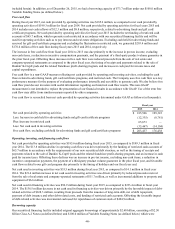

We received net proceeds at closing of the securitized financing facility of approximately $615 million, after giving effect to

the repayment of the remaining principal outstanding and interest on the term loans, payment of debt issuance costs and other

debt-related costs, as well as funding certain restricted cash accounts required under our securitized financing facility. The net

proceeds have been used for share repurchases, as further discussed below.

In connection with the January 2015 securitization refinancing, our board of directors authorized a new program to repurchase

up to an aggregate of $700.0 million of our outstanding common stock within the next two years. In February 2015, we entered

into an accelerated share repurchase agreement (the “February 2015 ASR Agreement”) with a third-party financial institution.

Pursuant to the terms of the February 2015 ASR Agreement, we paid the financial institution $400.0 million in cash and

received a delivery of 8,226,297 shares based on a weighted average cost per share of $48.62 over the term of the agreement.

In October 2015, we entered into a $125.0 million accelerated share repurchase agreement (the “October ASR Agreement”)

with a financial institution. Pursuant to the terms of the October ASR Agreement, we paid the financial institution $125.0

million from cash on hand and received an initial delivery of 2,527,167 shares, representing an estimate of 80% of the total

shares expected to be delivered under the October ASR Agreement. At settlement, the financial institution may be required to

deliver additional shares of common stock to us or, under certain circumstances, we may be required to deliver shares of our

common stock or may elect to make a cash payment to the financial institution. Upon the final settlement of the October ASR

Agreement, subsequent to fiscal year 2015, we received an additional delivery of 483,913 shares of its common stock based on

a weighted average cost per share of $41.51 over the term of the October ASR agreement.

Additionally, during the fiscal year 2015 we used $100.0 million to repurchase shares in the open market.

In February 2016, our board of directors increased the availability under the existing share repurchase program to $200.0

million of outstanding shares of our common stock. This repurchase authorization expires two years from the date of such

increase. In February 2016, we entered into an accelerated share repurchase agreement (the “February 2016 ASR Agreement”)

with a third-party financial institution. Pursuant to the terms of the February 2016 ASR Agreement, we paid the financial

institution $30.0 million from cash on hand and received an initial delivery of 553,506 shares, representing an estimate of 80%

of the total shares expected to be delivered under the February 2016 ASR Agreement. At settlement, the financial institution

may be required to deliver additional shares of common stock to us or, under certain circumstances, the Company may be