HSBC 2011 Annual Report Download - page 354

Download and view the complete annual report

Please find page 354 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

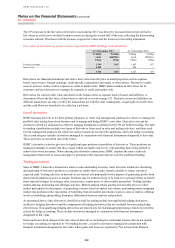

16 – Fair values of financial instruments carried at fair value

352

model and the assumptions relating to prepayment speeds, default rates and loss severity based on collateral type, and

performance, as appropriate. The valuations output is benchmarked for consistency against observable data for

securities of a similar nature.

Loans, including leveraged finance and loans held for securitisation

Loans held at fair value are valued from broker quotes and/or market data consensus providers when available. In the

absence of an observable market, the fair value is determined using valuation techniques. These techniques include

discounted cash flow models, which incorporate assumptions regarding an appropriate credit spread for the loan,

derived from other market instruments issued by the same or comparable entities.

Structured notes

The fair value of structured notes valued using a valuation technique is derived from the fair value of the underlying

debt security, and the fair value of the embedded derivative is determined as described in the paragraph below

on derivatives.

Trading liabilities valued using a valuation technique with significant unobservable inputs principally comprised

equity-linked structured notes, which are issued by HSBC and provide the counterparty with a return that is linked to

the performance of certain equity securities, and other portfolios. The notes are classified as Level 3 due to the

unobservability of parameters such as long-dated equity volatilities and correlations between equity prices, between

equity prices and interest rates and between interest rates and foreign exchange rates.

Derivatives

OTC (i.e. non-exchange traded) derivatives are valued using valuation models. Valuation models calculate the

present value of expected future cash flows, based upon ‘no-arbitrage’ principles. For many vanilla derivative

products, such as interest rate swaps and European options, the modelling approaches used are standard across the

industry. For more complex derivative products, there may be some differences in market practice. Inputs to

valuation models are determined from observable market data wherever possible, including prices available from

exchanges, dealers, brokers or providers of consensus pricing. Certain inputs may not be observable in the market

directly, but can be determined from observable prices via model calibration procedures or estimated from historical

data or other sources. Examples of inputs that may be unobservable include volatility surfaces, in whole or in part, for

less commonly traded option products, and correlations between market factors such as foreign exchange rates,

interest rates and equity prices. The valuation of derivatives with monolines is discussed on page 154.

Derivative products valued using valuation techniques with significant unobservable inputs included certain types of

correlation products, such as foreign exchange basket options, equity basket options, foreign exchange interest rate

hybrid transactions and long-dated option transactions. Examples of the latter are equity options, interest rate and

foreign exchange options and certain credit derivatives. Credit derivatives include certain tranched CDS transactions.