Progress Energy 2009 Annual Report Download - page 202

Download and view the complete annual report

Please find page 202 of the 2009 Progress Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

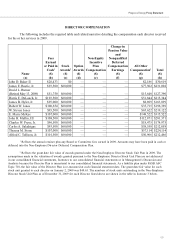

PROXY STATEMENT

64

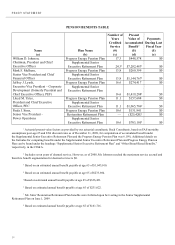

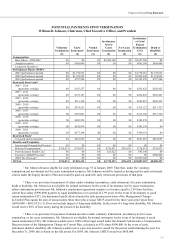

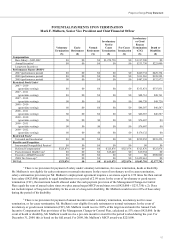

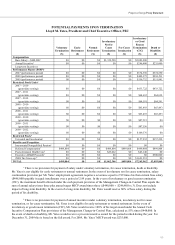

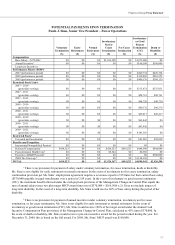

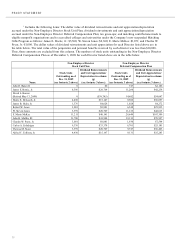

3 Unvested performance shares would be forfeited under voluntary termination, involuntary not for cause termination,

or for cause termination. Mr. Lyash is not eligible for early retirement or normal retirement. In the event of involuntary or good

reason termination (CIC), unvested performance shares vest as of the date of Management Change-in-Control and payment is

made based upon the applicable performance factor. As of December 31, 2009, the performance factor is 100%. In the event

of death or disability, the 2007 performance shares would vest 100% and be paid in an amount using performance factors

determined at the time of the event. For the 2008 and 2009 performance grants, a pro-rata payment would be made based upon

time in the plan.

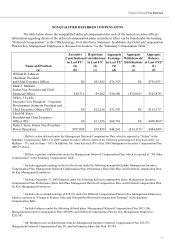

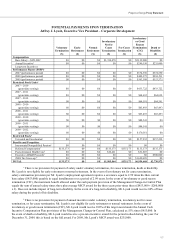

4 Unvested restricted stock units (RSU) would be forfeited under voluntary termination, involuntary not for cause

termination, or for cause termination. Mr. Lyash is not eligible for early retirement or normal retirement. In the event of

involuntary or good reason termination (CIC), all outstanding restricted stock units would vest immediately. For a detailed

description of outstanding restricted stock units, see the “Outstanding Equity Awards at Fiscal Year-End Table.” Upon death or

disability, all outstanding restricted stock units that are more than one year past their grant date would vest immediately. Shares

that are less than one year past their grant date would be forfeited. Mr. Lyash would immediately vest 13,727 restricted stock

units granted on March 20, 2007; 3,194 restricted stock units granted on March 18, 2008; and would forfeit 8,477 restricted stock

units granted on March 17, 2009.

5 Unvested restricted stock would be forfeited under voluntary termination, involuntary not for cause termination, or for

cause termination. Mr. Lyash is not eligible for early retirement or normal retirement. In the event of involuntary or good reason

termination (CIC), all outstanding restricted stock shares would vest immediately. For a detailed description of outstanding

restricted stock shares, see the “Outstanding Equity Awards at Fiscal Year-End Table.” Upon death or disability, all outstanding

restricted stock shares that are more than one year past their grant date would vest immediately. Shares that are less than one

year past their grant date would be forfeited. All of Mr. Lyash’s restricted stock grant dates are beyond the one-year threshold;

therefore, all 3,834 restricted stock shares would vest immediately.

6 No accelerated vesting or incremental nonqualified pension benefit applies under any of these scenarios. Mr. Lyash

was vested under the SERP as of December 31, 2009, so there is no incremental value due to accelerated vesting under

involuntary or good reason termination (CIC).

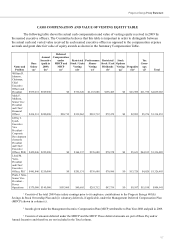

7 All outstanding deferred compensation balances will be paid immediately following termination, subject to IRC

Section 409(a) regulations, under voluntary termination, involuntary not for cause termination, for cause termination, involuntary

or good reason termination (CIC), death and disability. Mr. Lyash is not eligible for early retirement or normal retirement.

Unvested MICP deferral premiums would be forfeited. Mr. Lyash would forfeit $0 of unvested deferred MICP premiums.

8 No post-retirement health care benefits apply under voluntary termination, for cause termination, death or disability.

Mr. Lyash is not eligible for early retirement or normal retirement. Under involuntary not for cause termination, Mr. Lyash would

be reimbursed for 18 months of COBRA premiums at $901.19 per month as provided in his employment agreement. In the event

of involuntary or good reason termination (CIC), the Management Change-in-Control Plan provides for Company-paid medical,

dental and vision coverage in the same plan Mr. Lyash was participating in prior to termination for 36 months at $883.52 per

month.

9 Mr. Lyash would be eligible to receive $500,000 proceeds from the executive AD&D policy.

10 Upon a change in control, the Management Change-in-Control Plan provides for the Company to pay all excise taxes

under IRC Section 280G plus applicable gross-up amounts for Mr. Lyash. Under IRC Section 280G, Mr. Lyash would be subject

to excise tax on $2,988,788 of excess parachute payments above his base amount. Those excess parachute payments result in

$597,758 of excise taxes, $999,777 of tax gross-ups, and $23,164 of employer Medicare tax related to the excise tax payment.