AT&T Wireless 2007 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2007 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

2007 AT&T Annual Report

| 43

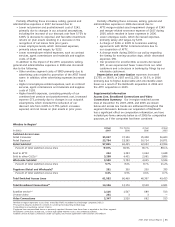

that reflect our judgment of the probable outcome of tax

contingencies (see Note 10). In 2007, we adopted Financial

Accounting Standards Board Interpretation No. 48,

“Accounting for Uncertainty in Income Taxes” (FIN 48) and

began accounting for uncertain tax positions under the

provisions of FIN 48 (see Note 1). As required by FIN 48, we

use our judgment to determine whether it is more likely than

not that we will sustain positions that we have taken on tax

returns and, if so, the amount of benefit to initially recognize

within our financial statements. We regularly review our

uncertain tax positions and adjust our unrecognized tax benefits

in light of changes in facts and circumstances, such as changes

in tax law, interactions with taxing authorities and develop-

ments in case law. These adjustments to our unrecognized

tax benefits may affect our income tax expense. Settlement

of uncertain tax positions may require use of our cash.

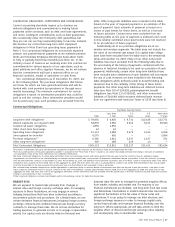

New Accounting Standards

FAS 141(R) In December 2007, the Financial Accounting

Standards Board (FASB) issued Statement of Financial

Accounting Standards No. 141 (revised 2007), “Business

Combinations” (FAS 141(R)). FAS 141(R) is a revision of

FAS 141 and requires that costs incurred to effect the

acquisition (i.e., acquisition-related costs) be recognized

separately from the acquisition. In addition, in accordance

with FAS 141, restructuring costs that the acquirer expected

but was not obligated to incur, which included changes to

benefit plans, were recognized as if they were a liability

assumed at the acquisition date. FAS 141(R) requires the

acquirer to recognize those costs separately from the business

combination. We are currently evaluating the impact that

FAS 141(R) has on our accounting for acquisitions prior to

the effective date of the first fiscal year beginning after

December 15, 2008.

FAS 159 In February 2007, the FASB issued Statement

of Financial Accounting Standards No. 159, “The Fair Value

Option for Financial Assets and Financial Liabilities” (FAS 159).

FAS 159 permits companies to choose to measure many

financial instruments and certain other items at fair value,

thereby providing the opportunity to mitigate volatility in

reported earnings caused by measuring related assets and

liabilities differently without having to apply complex hedge

accounting provisions. FAS 159 is effective for fiscal years

beginning after November 15, 2007. We elected not to

adopt the fair value option for valuation of those assets

and liabilities which are eligible, therefore there is no impact

on our financial position and results of operations.

FAS 160 In December 2007, the FASB issued Statement

of Financial Accounting Standards No. 160, “Noncontrolling

Interests in Consolidated Financial Statements, an amendment

of ARB No. 51” (FAS 160). FAS 160 requires noncontrolling

interests held by parties other than the parent in subsidiaries

be clearly identified, labeled, and presented in the

consolidated statement of financial position within equity,

but separate from the parent’s equity. FAS 160 is effective

for fiscal years beginning after December 15, 2008. We are

currently evaluating the impact FAS 160 will have on our

financial position and results of operations.

EITF 06-4 In March 2007, the Emerging Issues Task Force

(EITF) ratified the consensus on EITF 06-4, “Accounting for

Deferred Compensation and Postretirement Benefit Aspects

of Endorsement Split-Dollar Life Insurance Arrangements”

(EITF 06-4). EITF 06-4 covers endorsement split-dollar life

insurance arrangements (where the company owns and

controls the policy) and provides that an employer should

recognize a liability for future benefits in accordance with

Statement of Financial Accounting Standards No. 106,

“Employers’ Accounting for Postretirement Benefits Other

Than Pensions.” EITF 06-4 is effective for fiscal years

beginning after December 15, 2007. We are currently

evaluating the impact EITF 06-4 will have on our financial

position and results of operations.

EITF 06-11 In June 2007, the EITF ratified the consensus

on EITF 06-11, “Accounting for Income Tax Benefits of

Dividends on Share-Based Payment Awards” (EITF 06-11).

EITF 06-11 provides that a realized income tax benefit from

dividends or dividend equivalents that are charged to retained

earnings and are paid to employees for nonvested equity-

classified share-based awards and equity-classified

outstanding share options should be recognized as an

increase to additional paid-in capital rather than a reduction

of income tax expense. EITF 06-11 applies prospectively to

the income tax benefits that result from dividends on

equity-classified employee share-based payment awards

that are declared in fiscal periods beginning after

December 15, 2007. EITF 06-11 will not have a material

impact on our financial position and results of operations.

OTHER BUSINESS MATTERS

Spectrum Licenses In October 2007, we agreed to purchase

spectrum licenses covering 196 million people in the 700 MHz

frequency band from Aloha Partners, L.P. for $2,500. The

spectrum covers many major metropolitan areas, including

72 of the top 100 and all of the top 10 markets in the U.S.

We closed this transaction in February 2008. Additionally,

we are an eligible bidder in the FCC wireless spectrum

auctions which began in January 2008.

Spectrum Sale In February 2007, we agreed to sell to

Clearwire Corporation (Clearwire), a national provider of

wireless broadband Internet access, education broadband

service spectrum and broadband radio service spectrum

valued at $300. The transaction received the necessary

regulatory approvals and closed in May 2007. Sale of this

spectrum was required as a condition to the approval of

our acquisition of BellSouth.

Antitrust Litigation In 2002, two consumer class-action

antitrust cases were filed in the United States District Court

for the Southern District of New York (District Court) against

SBC Communications Inc., Verizon, BellSouth and Qwest

Communications International Inc. alleging that they have

violated federal and state antitrust laws by agreeing not to

compete with one another and acting together to impede

competition for local telephone services (Twombly v. Bell

Atlantic Corp., et al.). In October 2003, the District Court

granted the joint defendants’ motion to dismiss and the

plaintiffs appealed. In October 2005, the United States Court

of Appeals for the Second Circuit Court (Second Circuit)

reversed the District Court, thereby allowing the cases to

proceed. In June 2006, the Supreme Court of the United

States (Supreme Court) announced its decision to review the

case. In May 2007, the Supreme Court reversed the Second

Circuit’s decision and remanded the case to the Second Circuit

for further proceedings consistent with its opinion; we are

awaiting formal dismissal of the case.