AT&T Wireless 2007 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2007 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

|

|

2007 AT&T Annual Report

| 73

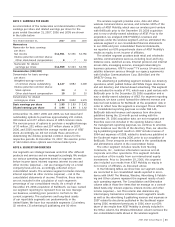

Net Periodic Benefit Cost and Other Amounts Recognized in Other Comprehensive Income

Our combined net pension and postretirement cost recognized in our consolidated statements of income was $1,078, $1,635 and

$1,336 for the years ended December 31, 2007, 2006 and 2005.

The following tables present the components of net periodic benefit obligation cost and other changes in plan assets and

benefit obligations recognized in other comprehensive income:

Net Periodic Benefit Cost

Pension Benefits Postretirement Benefits

2007 2006 2005 2007 2006 2005

Service cost – benefits earned during the period $ 1,257 $ 1,050 $ 804 $ 511 $ 435 $ 390

Interest cost on projected benefit obligation 3,220 2,507 1,725 2,588 1,943 1,496

Expected return on plan assets (5,468) (3,989) (2,736) (1,348) (935) (781)

Amortization of prior service cost (benefit) and transition asset 142 149 186 (359) (359) (344)

Recognized actuarial loss 241 361 156 294 473 440

Net pension and postretirement cost (benefit)1 $ (608) $ 78 $ 135 $ 1,686 $1,557 $1,201

1 During 2007, 2006 and 2005, the Medicare Prescription Drug, Improvement and Modernization Act of 2003 reduced postretirement benefit cost by $342, $349 and $304. This effect is

included in several line items above.

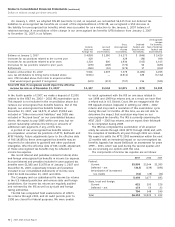

Other Changes in Plan Assets and Benefit Obligations Recognized in Other Comprehensive Income

Pension Benefits Postretirement Benefits

2007 2006 20051 2007 2006 20051

Net loss (gain) $(2,131) $2,650 $ — $(2,525) $ 3,404 $ —

Prior service cost (credit) 139 387 — (28) (1,655) —

Amortization of net loss (gain) 154 — — 181 — —

Amortization of prior service cost 78 — — (223) — —

Total recognized in net pension and postretirement cost

other comprehensive income $(1,760) $3,037 $ — $(2,595) $ 1,749 —

1FAS 158 required prospective application for fiscal years ending after December 15, 2006.

The estimated net loss and prior service cost for pension

benefits that will be amortized from accumulated other

comprehensive income into net periodic benefit cost over the

next fiscal year are $7 and $134, respectively. The estimated

prior service benefit for postretirement benefits that will be

amortized from accumulated other comprehensive income

into net periodic benefit cost over the next fiscal year is $360.

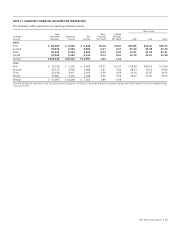

Assumptions

In determining the projected benefit obligation and the net

pension and postemployment benefit cost, we used the

following significant weighted-average assumptions:

2007 2006 2005

Discount rate for determining

projected benefit obligation

at December 31 6.50% 6.00% 5.75%

Discount rate in effect for

determining net cost (benefit)1 6.00% 5.75% 6.00%

Long-term rate of return

on plan assets 8.50% 8.50% 8.50%

Composite rate of compensation

increase for determining

projected benefit obligation

and net pension cost (benefit) 4.00% 4.00% 4.00%

1

Discount rate in effect for determining net cost (benefit) of BellSouth and AT&T Mobility

pension and postretirement plans for the two-day period ended December 31, 2006, was

6.00%. The discount rate in effect for determining net cost (benefit) of ATTC pension and

postretirement plans for the 43-day period ended December 31, 2005 was 5.75%.

Approximately 10% of pension and postretirement costs are

capitalized as part of construction labor, providing a small

reduction in the net expense recorded. While we will continue

our cost-control efforts, certain factors, such as investment

returns, depend largely on trends in the U.S. securities

markets and the general U.S. economy. In particular,

uncertainty in the securities markets and U.S. economy could

result in investment returns less than those assumed and a

decline in the value of plan assets used in pension and

postretirement calculations, which under GAAP we will

recognize over the next several years. Should the securities

markets decline or medical and prescription drug costs increase

at a rate greater than assumed, we would expect increasing

annual combined net pension and postretirement costs for the

next several years. Additionally, should actual experience

differ from actuarial assumptions, combined net pension and

postretirement cost would be affected in future years.

Discount Rate Our assumed discount rate of 6.50% at

December 31, 2007 reflects the hypothetical rate at which

the projected benefit obligations could be effectively settled

or paid out to participants on that date. We determined our

discount rate based on a range of factors, including a yield

curve comprised of the rates of return on high-quality,

fixed-income corporate bonds available at the measurement

date and the related expected duration for the obligations.

For the year ended December 31, 2007, we increased our

discount rate by 0.50%, resulting in a decrease in our pension

plan benefit obligation of $2,353 and a decrease in our