American Airlines 2004 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2004 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

22

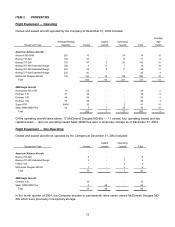

LIQUIDITY AND CAPITAL RESOURCES

Cash, Short-Term Investments, Restricted Assets and Deposits

At December 31, 2004, the Company had $2.9 billion in unrestricted cash and short-term investments and $478

million in restricted cash and short-term investments.

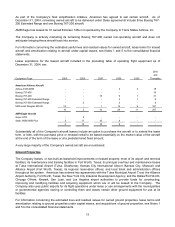

Significant Indebtedness and Future Financing

During 2002, 2003 and 2004, in addition to refinancing its $834 million credit facility (see discussion in Note 6 to

the consolidated financial statements), the Company raised an aggregate of approximately $6.0 billion of financing,

mostly to fund capital commitments (mainly for aircraft and ground properties) and operating losses. As of the date

of this Form 10-K, the Company believes that it should have sufficient liquidity to fund its operations for the

foreseeable future, including repayment of debt and capital leases, capital expenditures and other contractual

obligations. However, to maintain sufficient liquidity as the Company continues to implement its restructuring and

cost reduction initiatives, and because the Company has significant debt obligations maturing in the next several

years, as well as substantial pension funding obligations, the Company will need access to additional funding. The

Company’s possible financing sources primarily include: (i) a limited amount of additional secured aircraft debt (a

very large majority of the Company’s owned aircraft, including virtually all of the Company’s Section 1110-eligible

aircraft, are encumbered) or sale-leaseback transactions involving owned aircraft, (ii) debt secured by new aircraft

deliveries, (iii) debt secured by other assets, (iv) securitization of future operating receipts, (v) the sale or

monetization of certain assets, (vi) unsecured debt and (vii) equity and/or equity-like securities. However, the

availability and level of these financing sources cannot be assured, particularly in light of the Company’s and

American’s reduced credit ratings, high fuel prices, historically weak revenues and the financial difficulties being

experienced in the airline industry. The inability of the Company to obtain additional funding would have a material

negative impact on the ability of the Company to sustain its operations over the long-term.

The Company’s substantial indebtedness could have important consequences. For example, it could (i) limit the

Company’s ability to obtain additional financing for working capital, capital expenditures, acquisitions and general

corporate purposes, or adversely affect the terms on which such financing could be obtained; (ii) require the

Company to dedicate a substantial portion of its cash flow from operations to payments on its indebtedness,

thereby reducing the funds available for other purposes; (iii) make the Company more vulnerable to economic

downturns; (iv) limit its ability to withstand competitive pressures and reduce its flexibility in responding to changing

business and economic conditions; and (v) limit the Company’s flexibility in planning for, or reacting to, changes in

its business and the industry in which it operates.

Credit Ratings

AMR’s and American’s credit ratings are significantly below investment grade. Additional reductions in AMR's or

American's credit ratings could further increase its borrowing or other costs and further restrict the availability of

future financing.

Credit Facility Covenants

On December 17, 2004, American refinanced its $834 million bank credit facility, which was scheduled to mature

in December 2005. The total amount of the new credit facility is $850 million, all of which has been borrowed by

American. The new credit facility consists of a $600 million senior secured revolving credit facility, with a final

maturity on June 17, 2009, and a $250 million term loan facility, with a final maturity on December 17, 2010 (the

Revolving Facility and the Term Loan Facility, respectively, and collectively, the Credit Facility). American’s

obligations under the Credit Facility are guaranteed by AMR.