Bank of America 2000 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2000 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

12

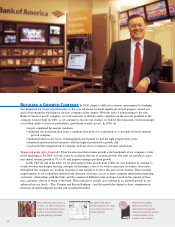

Serving Consumers

Our franchise is the envy of the industry and

our relationship strategy rewards customers for

allowing us to do more for them and grow revenue

when they bring us more of their business.

Suppose you could have unlimited access to the entire global payments system, enabling you to move funds anywhere

you needed them, day or night, to or from anybody, through any channel you want: in person, at a machine on a

street corner, on the phone, even sitting at a PC in your kitchen. We would maintain those access channels at our

expense. We would also keep your money safe. You could get to it whenever you wanted, but nobody else could touch

it without your consent. And we’d do all the bookkeeping; you would only have to check your balance periodically.

Sound like a useful service? Actually, it’s a simple checking account. It comes in different shapes and sizes to

fit different needs, with flexible pricing, depending on how you choose to use it. That’s where it all starts.

Where it goes from there is up to the customer. We are integrating the products and services we provide –

checking and savings accounts, investment products, loans, across our various delivery channels, including banking

centers, ATMs, relationship managers, telephones, personal computers and hand-held devices – to make it easy and

convenient for customers to expand their relationships with us. When customers bring us more of their business, we

earn more revenue, which enables us to provide them with a value package that might include such benefits as pre-

ferred pricing, reduced fees, higher interest rates on deposits, flexible credit terms and dedicated phone lines staffed

by specially trained associates.

At the same time, we are investing heavily in improving the quality of our baseline service. For example, we

have shortened the hold time on deposited checks and reduced the volume of holds on non-cash deposits at ATMs.

We have also simplified our phone systems, making it quicker and easier for customers to get their questions answered

and problems solved. In fact, in a survey of 18 banks, three of our Contact Centers placed first, second and third in

service quality. As a result, our customer satisfaction scores have improved in most of our markets over the past year.

We have clearly defined levels of relationship service for individuals and families, including our Private Bank,

whose very affluent customers require top-quality advice in managing their relatively complex financial affairs.

Premier clients are consumers who qualify, on the basis of income and the size of their relationship, for customized

personal service.

Unparalleled Customer Convenience

4,500 banking centers

13,000 ATMs

1,500,000 daily phone inquiries

3,000,000 online customers

7,000,000 customer touches per day