Bank of America 2000 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2000 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

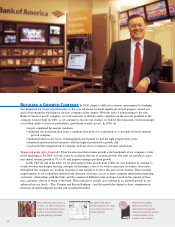

Card and Payment Services

Bank of America is investing in its card and

payments business to build upon already-

impressive growth across all card-related

businesses and customer segments. For 2000,

consumer credit and debit card sales volumes

were up 17%, and commercial card volume

was up more than 30%.

Card’s strong growth is being fueled by

several factors. First, cards have become the

preferred way to pay. For businesses, purchas-

ing cards are a far more efficient way to pay

suppliers. For consumers, cards are the domi-

nant form of payment on the Internet, and

nothing matches the convenience and control

that cards offer both online and at physical

points of sale. By 2005, cards are projected to

overtake checks as the most used form of

payments for consumers.

Bank of America is leading this paper-

to-plastic payments revolution, primarily by

leveraging and deepening customer relation-

ships across all lines of business.

Like many card companies, the bank is

making significant investments in marketing

and new products. Direct mail solicitations have

doubled, as have new accounts from that source.

Bank of America has launched “Photo Security”

credit cards, upgraded Check Cards and intro-

duced the new Visa BuxxTM card for teenagers,

enabling parents to program value into the card

and monitor purchases. A newly integrated

national sales force is selling unique bundled

products to meet the needs of small business

and middle market customers.

Unlike many other card companies,

Bank of America can leverage its huge base

of banking relationships to produce a higher

return on its investment. For example, the

bank is soliciting twice as many relationship

customers as in the past because these cus-

tomers have almost 30% higher response

rates to card solicitations and 25% lower

overall loss rates. The bank’s mailing “uni-

verse” has been increased 50%, and the cost

of acquiring a new account is down by

more than 30%.

Customer relationship information is

also a key to improving customer satisfaction

and operational performance. For example,

lower-risk relationship customers don’t need

to be called when their payments are only a

few days overdue. Attention can be focused

on higher-risk accounts, thereby increasing

collections effectiveness and improving cus-

tomer satisfaction.

Customers are also getting an enhanced

Check Card experience as the bank’s ability

to use relationship information grows. Lower-

risk customers are now identified and their

transactions approved, allowing them to use

their cards to fund purchases directly from

their accounts, even when their balances run

low. Revenue is projected to increase

sharply as a result, and customer satisfaction

will benefit from fewer declined transactions.

Card products can also be a good way to

create new banking relationships. Thousands

of single-service credit card customers are

expanding their relationships with the bank,

and when single-service customers become

relationship customers, their relationship net

income increases more than 600 percent.

Harnessing customer information that

no other card company possesses, the bank

is leveraging the value of relationships to

improve both the customer experience and

financial performance.

15

The Bank of America Check CardTM

is becoming increasingly popu-

lar with customers, and it's

easy to see why. Check Cards

offer the point-of-sale conven-

ience of a credit card, but reduce

the need to write checks or carry

cash for everyday purchases.

This popularity is reflected

in our large increase in Check

Card purchase volume, which

was up 28% in 2000. Per-card

transactions are also rising,

another sign that customers like

the convenience of the Bank of

America Check Card.

Higher transaction volumes

mean higher revenue for Bank

of America, as well as lower

processing and servicing costs

than we incur when customers

write checks or withdraw cash

from ATMs. From 1998 through

2000, debit card revenue has

more than doubled, from $225

million to $520 million.

As more of our products

migrate from paper to electronic

channels, we will continue to

grow revenues and reduce costs,

while providing better service

and convenience for customers.