Bank of America 2000 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2000 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

13

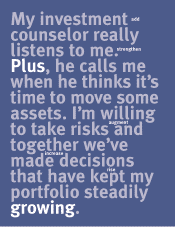

But the largest and fastest grow-

ing group of relationship customers

are those we call Plus. These indi-

viduals qualify for enhanced service

simply because of the volume of busi-

ness they bring to the bank, not by

income level or any other demo-

graphic measure. Almost anyone can

qualify by simply maintaining an

account such as Advantage or the

Money Manager Account, which

combine investment and banking,

or by combining a checking account

with a home loan. We are able to

provide an attractive value package

to Plus customers because we receive

considerable value in return. The rate

of customer retention increases

12% when customers move to Plus.

Deposit, investment and credit bal-

ances all tend to grow rapidly. And

the net income we derive from the

relationship increases significantly.

Imagine how revenue and prof-

its would grow if the millions of

customers who qualify for Plus or

Premier service, or for the Private

Bank, would sign up for one of

those service levels.

And we have additional oppor-

tunities to grow our revenue, simply

by doing more for our customers

who already enjoy relationship serv-

ice. For example, Plus customers

average 10 financial relationships

per household, although typically

only four of those are with Bank of

America. They have nearly three times

the appetite for credit as the general

population, and they save and invest

at five times the average rate. Yet they

take much of their credit and invest-

ment business to other financial insti-

tutions, most of which we believe

cannot match our convenience or

provide the broad complement of

financial services we can.

Two of our biggest growth

engines, Asset Management and

Card and Payment Services, also

have tremendous potential for

advancing our relationship strategy

(see pages 14-15).

Another area with strong rela-

tionship potential is consumer real

estate, where we have made huge

strides in improving our quality of

service. As the nation’s largest ser-

vicer and third-largest originator of

home mortgages, Bank of America

helps more than 400,000 families

fulfill their dreams of home owner-

ship each year. This is a business in

which razor-thin margins and heavy

competition make it essential to main-

tain a low-cost, high-quality environ-

ment. By redesigning the application,

approval and delivery process for

telephone lending, we have shaved

several days off the time it takes us

to move from a loan application to

a booking, increased our mortgage

approval rate by 15% and raised our

booking rate nearly 30%.

We view our nationwide con-

sumer franchise as the envy of the

industry and the most convenient

for customers. The states in which

Bank of America offers full-service

banking account for 80% of the

nation’s projected population growth

over the next five years, and we have

the leading market share in the four

fastest growing states.

Achieving our growth goals is

easier said than done. But we know

we can succeed because we are

already doing it in some key busi-

nesses, such as Asset Management

and Card and Payment Services and

in some markets. In California, our

largest market by far, we grew rev-

enues 8% in 2000. Deposits grew

7.4% and consumer assets grew more

than 12%. Those growth rates are

significantly higher than the year

before. We intend to continue to

improve the integration of our prod-

ucts and services across all delivery

channels with the goal of getting

the rest of the consumer franchise

to perform at least at that level.

When we do that, we will have

transformed Bank of America into a

truly great growth company.

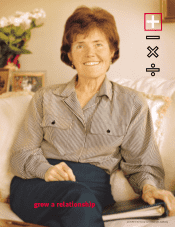

Janet Hill of Danville, California, is a

savvy investor whose portfolio repre-

sents a significant portion of her income.

Actively involved in her family’s finan-

cial decision-making since her two

daughters were young, she and her

husband took many investment

courses over the years and belonged

to an investment club.

Widowed four years ago, Hill

looked for an investment counselor

who respected her experience and

input. She found the person she was

looking for at Bank of America. “We

talk regularly – either he calls me or I

call him – and we meet three or four

times a year,” she said. Hill’s relation-

ship with the bank also includes check-

ing and savings accounts, credit cards

and an IRA. A volunteer for the Red

Cross and programs for disadvantaged

children, she and her daughter recently

bought a horse, and she intends to

take riding lessons. Confident her

portfolio is in capable hands, Hill

makes the most of her very full life.