Charter 2000 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2000 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32

|

|

CHARTER COMMUNICATIONS 20CHARTER COMMUNICATIONS 20

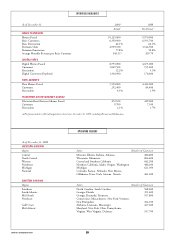

FINANCIAL HIGHLIGHTS

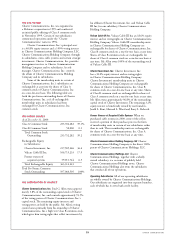

RECENT ACQUISITIONS

Acquisition summary

Since January 1, 1999, we have completed sixteen acquisi-

tions for a total purchase price of $14.3 billion consisting

of cash payments of $9.1 billion, $3.3 billion of assumed

debt and $1.9 billion of equity interests issued. These

acquisitions were funded through the issuance of stock and

long-term debt, bank borrowings and internally generated

funds. All acquisitions were accounted for under the pur-

chase method of accounting and results of operations were

included in our consolidated financial statements from the

respective dates of acquisition.

Acquisition Acquired

Company Date Customers

Renaissance 4/99 134,000

American Cable 5/99 69,000

Greater Media Systems 6/99 176,000

Helicon 7/99 171,000

Vista 7/99 26,000

Cable Satellite 8/99 9,000

Rifkin 9/99 463,000

InterMedia 10/99 278,000

Fanch 11/99 535,600

Falcon 11/99 977,200

Avalon 11/99 270,800

Interlake 1/00 6,000

Bresnan 2/00 695,800

Capital Cable 4/00 23,200

Farmington Cablevision 4/00 5,700

Cablevision of Michigan 9/00 50,700

Total Acquisitions 3,891,000

Pending AT&T transactions

In February 2001, we entered into several agreements with

AT&T Broadband, LLC involving several strategic cable

system transactions that will result in a net addition of

approximately 512,000 customers for the Charter cable

systems. We expect to acquire cable systems from AT&T

Broadband serving approximately 574,000 customers in

Missouri, Alabama, Nevada and California for a total of

$1.79 billion. A portion of the purchase price will consist

of Charter cable systems valued at $249.0 million serving

approximately 62,000 customers in Florida, resulting in

a net addition of 512,000 customers. Of the balance of

the purchase price, up to $501.5 million will be paid in

Class A common stock and the remainder will be paid

in cash. Charter Communications Holdings, LLC and its

subsidiary Charter Communications Holdings Capital

Corporation have a commitment for a loan from Morgan

Stanley Senior Funding, Inc. and Goldman Sachs Credit

Partners LP for temporary financing of the cash portion

of the purchase price. We expect to obtain permanent

financing through one or more debt or equity financing

transactions or a combination thereof. The acquisition

transactions are expected to close in the second and/or

third quarters of 2001, subject to certain closing condi-

tions and regulatory review.

OVERVIEW OF OPERATIONS

Approximately 87% of our revenues for the year ended

December 31, 2000 are attributable to monthly subscrip-

tion fees charged to customers for our basic, expanded

basic, premium and digital cable television programming

services, Internet access through television-based service,

dial-up telephone modems and high-speed cable modem

service, equipment rental and ancillary services provided

by our cable systems. The remaining 13% of revenues is

derived from installation and reconnection fees charged to

customers to commence or reinstate service, pay-per-view

programming, where users are charged a fee for individual

programs requested, advertising revenues and commissions

related to the sale of merchandise by home shopping serv-

ices and franchise revenues. We have generated increased

revenues in each of the past three years, primarily through

customer growth from acquisitions, internal customer

growth, basic and expanded tier rate increases and revenues

from new services and products.

Our expenses primarily consist of operating costs,

general and administrative expenses, depreciation and

amortization expense, interest expense and management

fees/corporate expense charges. Operating costs primarily

include programming costs, cable service related expenses,

marketing and advertising costs, franchise fees and

expenses related to customer billings.

We have had a history of net losses and expect to

continue to report net losses for the foreseeable future.

The principal reasons for our prior and anticipated net

losses include depreciation and amortization expenses

associated with our acquisitions and capital expenditures

related to the construction and upgrading of our systems,

and interest costs on borrowed money. We cannot predict

what impact, if any, continued losses will have on our

ability to finance our operations in the future.

FISCAL 2000 COMPARED TO FISCAL 1999

Revenues Revenues increased by $1,821.0 million or

127% from $1,428.2 million in 1999 to $3,249.2 million

in 2000. System operations acquired after January 1, 1999

accounted for $1,578.3 million or 87% of the increase

in 2000, while systems acquired before January 1, 1999

accounted for $242.7 million or 13%.

In 2000, we added 898,300 basic customers, growing

from 5,452,600 to 6,350,900, of which approximately

741,100 were the result of acquisitions. The remaining

157,200 relate to internal growth, which is an increase

of approximately 2.5% compared to the prior year on

a pro forma basis.

Premium units increased by 2,094,700 from

2,844,400 to 4,939,100, of which approximately

300,100 were a result of acquisitions. The remaining

increase of 1,794,600 is the result of aggressive marketing

and pricing of premium products related to upgrades.

In 2000, we added 943,300 digital customers,

growing from 126,200 to 1,069,500. Of the total increase,

approximately 29,200 were the result of acquisitions and

914,100 were the result of internal growth or upgrades.

The pace of growth increased throughout the year as we

upgraded our systems. We surpassed our expectations

throughout the year, with an average of 17,500 digital

installations per week during 2000 which increased to

40,000 digital installations per week in December 2000.

Growth was a result of intense marketing efforts and

strong demand for digital service.