DTE Energy 2010 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2010 DTE Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39

|

|

33

Assumptions used in determining the projected benefit obligation and net benefit cost are listed below:

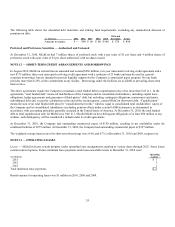

2010

2009

2008

Projected benefit obligation

Discount rate

5.50%

5.90%

6.90%

Net benefit costs

Discount rate

5.90%

6.90%

6.50%

Expected long-term rate of return on plan assets

8.75%

8.75%

8.75%

Health care trend rate pre-65

7.00%

7.00%

7.00%

Health care trend rate post-65

7.00%

7.00%

6.00%

Ultimate health care trend rate

5.00%

5.00%

5.00%

Year in which ultimate reached

2016

2016

2011

A one percentage point increase in health care cost trend rates would have increased the total service cost and interest cost components

of benefit costs by $7 million and increased the accumulated benefit obligation by $54 million at December 31, 2010. A one

percentage point decrease in the health care cost trend rates would have decreased the total service cost and interest cost components

of benefit costs by $7 million and would have decreased the accumulated benefit obligation by $80 million at December 31, 2010.

At December 31, 2010, the benefits expected to be paid, including prescription drug benefits, in each of the next five years and in the

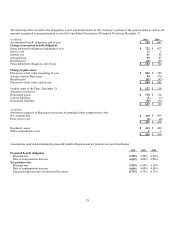

aggregate for the five fiscal years thereafter are as follows:

(in Millions)

2011

$ 27

2012

27

2013

32

2014

34

2015

35

2016 - 2020

196

Total

$ 351

The process used in determining the long-term rate of return for assets and the investment approach for our other postretirement

benefits plans is similar to those previously described for our pension plans.

In December 2003, the Medicare Act was signed into law which provides for a non-taxable federal subsidy to sponsors of retiree

health care benefit plans that provide a benefit that is at least “actuarially equivalent” to the benefit established by law. The effects of

the subsidy reduced net periodic postretirement benefit costs by $2 million in 2010, $4 million in 2009, and $3 million in 2008.

Change in plan assets

2010

2009

Plan assets at fair value, beginning of year

$ 270

$ 118

Company contributions

70

115

Actual return on plan assets

32

37

Benefits paid

(26)

—

Plan assets at fair value, end of year

$ 346

$ 270

Funded status at fair value, December 31

$ (182)

$ (218)

Noncurrent liabilities

$ (182)

$ (218)

Amounts recognized in regulatory assets

Net loss

$ 158

$ 136

Prior service cost (credit)

(8)

2

Net transition obligation

2

12

Regulatory Asset — postretirement costs

$ 152

$ 150