HSBC 2007 Annual Report Download - page 223

Download and view the complete annual report

Please find page 223 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

221

the greatest home value depreciation, driven by

rising unemployment rates in these markets and a

weakening US economy.

In vehicle finance, two months or more

delinquencies moved from 3.16 per cent at the end

of 2006 to 3.68 per cent at 31 December 2007. The

increased delinquency in the vehicle finance

portfolio was not as severe as has been experienced

elsewhere in the industry. In 2007, the vehicle

finance business tightened underwriting criteria in

both the dealer and direct-to-consumer channels, to

convert the mix of new loans to a higher credit

quality.

HSBC has been proactive in reaching out to

customers to provide financial counselling and

assist them in restructuring their debts to avoid

foreclosure. As a consequence, HSBC restructured

and modified loans that it believed could be

serviced, in line with local policies. In particular,

customers with ARM loans approaching the first

reset were contacted in order to assess their ability

to make the higher payments and, where

appropriate, to refinance or modify their loans.

As a result, in 2007 HSBC has modified more

than 8,500 loans with an aggregate balance of more

than US$1.4 billion.

In 2007, approximately US$4.5 billion of

ARM loans reached their first interest rate reset.

In 2008, approximately US$6.5 billion of ARMs

will reach their first interest rate reset, of which

US$2.8 billion relates to HSBC Bank USA and

US$3.7 billion to HSBC Finance. Within the latter,

US$2.7 billion is in mortgage services, the

remainder in consumer lending. ARMs in HSBC

Bank USA are largely prime balances. Delinquency

rates are expected to continue to rise in 2008, as the

limiting of originations means that the portfolio

will mostly be running off. A deterioration in

economic conditions and the housing market would

also increase delinquencies.

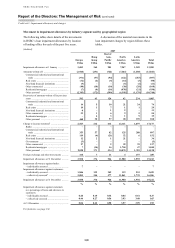

Loan delinquency in the US

(Unaudited)

The following tables provide a detailed analysis of

loan delinquency in the US.

Two months and over contractual delinquency in Personal Financial Services in the US

(Unaudited)

Quarter ended

31

December

2007

30

September

2007

30

June

2007

31

March

2007

31

December

2006

30

September

2006

30

June

2006

31

March

2006

US$m US$m US$m US$m US$m US$m US$m US$m

Residential mortgages1 .. 5,404 3,868 2,992 2,703 2,733 2,335 1,999 1,892

Second lien mortgage

lending1 ...................... 1,589 1,240 941 855 810 580 416 352

Vehicle finance2 ............. 488 451 384 302 415 421 367 292

Credit card ..................... 1,830 1,581 1,314 1,274 1,312 1,217 1,089 1,100

Private label ................... 598 536 434 429 471 444 419 373

Personal non-credit card 2,634 2,238 2,000 1,881 1,888 1,696 1,518 1,518

Total1 .............................. 12,543 9,914 8,065 7,444 7,629 6,693 5,808 5,527

%

3 %3 %

3 %

3 %

3 %

3 %3 %3

Residential mortgages1 .. 5.47 3.83 2.92 2.54 2.54 2.19 1.89 1.81

Second lien mortgage

lending1 ...................... 9.02 6.81 5.02 4.35 3.97 2.79 2.03 1.81

Vehicle finance2 ............. 3.68 3.40 2.91 2.29 3.16 3.21 2.82 2.27

Credit card ..................... 5.68 5.09 4.32 4.43 4.48 4.46 4.09 4.28

Private label ................... 3.43 3.28 2.72 2.65 2.83 2.88 2.84 2.60

Personal non-credit card 13.16 10.88 9.69 9.33 9.05 8.23 7.56 7.70

Total1 .............................. 6.29 4.95 4.00 3.64 3.67 3.28 2.89 2.81

1 Consumer lending balances for the first three quarters of 2006 have been restated due to a reclassification of balances between first lien

and second lien. Mortgage services balances for the second half of 2006 and the first half of 2007 have been restated due to a

reclassification of assets between foreclosed and second lien.

2 In December 2006, the vehicle finance business changed its write-off policy to provide that the principal balance of vehicle loans in

excess of the estimated net realisable value will be written off 30 days (previously 90 days) after the financed vehicle has been

repossessed if it remains unsold, unless it becomes 150 days contractually delinquent, at which time such excess will be written off. This

resulted in a one-time acceleration of write-offs totalling US$24 million in December 2006. In connection with this policy change, the

vehicle finance business also changed its methodology for reporting two months and over contractual delinquency to include loan

balances associated with repossessed vehicles which have not yet been written down to net realisable value. This resulted in an increase

of 42 basis points to the vehicle finance delinquency ratio and an increase of 3 basis points to the total consumer delinquency ratio.

3 Expressed as a percentage of loans and advances in Personal Financial Services in the US.