HSBC 2007 Annual Report Download - page 229

Download and view the complete annual report

Please find page 229 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

227

partly offset by a decline in the UK, where changes

in underwriting practices resulted in a fall in

personal unsecured lending in 2007.

In Hong Kong, impaired loans declined by

4 per cent to US$433 million. Credit conditions were

very favourable, reflecting the strong local economy

and buoyant equity and property markets.

In Rest of Asia-Pacific, the decline in impaired

loans of 11 per cent to US$1.1 billion was mainly

driven by lower impaired loans in Taiwan following

the non-recurrence of the effect of regulatory

changes which, in 2006, led to a significant increase

in impaired loans. This was partly offset by a rise in

impaired loans in India due to strong growth in

personal lending.

In North America, HSBC recorded a

73 per cent increase in impaired loans to

US$8.4 billion at 31 December 2007. The consumer

finance business in the US was responsible for the

bulk of the change. HSBC Finance experienced a

deterioration in credit quality in most of its lending

book, in particular for first and second lien

mortgages originated in 2005 and 2006. In the final

quarter of the year, in line with the market,

delinquencies rose in the credit card portfolio, with a

smaller rise in vehicle finance loans. A full

discussion of these developments and their effect on

credit quality is provided in the ‘Areas of special

interest’ commentary on page 216. In Canada,

although impaired loans rose from a low base, credit

conditions remained strong.

In Latin America, impaired loans increased by

30 per cent to US$2.1 billion, primarily due to a rise

of 76 per cent in impaired loans in Mexico. This was

due to portfolio growth, seasoning and higher

delinquency rates on credit cards. Revenues from

this growth in credit card lending more than covered

the rise in impairment charges.

Individually impaired loans and advances to customers

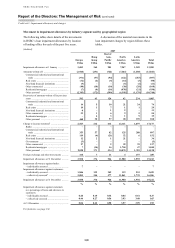

(Audited)

Europe

Hong

Kong

Rest of

Asia-

Pacific

North

America

Latin

America

Gross

impaired

loans and

advances to

customers

% of total

gross

impaired

loans1

US$m US$m US$m US$m US$m US$m %

At 31 December 2007

Individually impaired loans and

advances to customers:

– personal ............................... 1,073 178 225 68 4 1,548 23.9

– commercial and corporate ... 3,485 200 453 353 438 4,929 76.1

4,558 378 678 421 442 6,477 100.0

At 31 December 2006

Individually impaired loans and

advances to customers:

– personal ............................... 975 231 118 173 1 1,498

25.7

– commercial and corporate ... 3,056 176 531 248 324 4,335 74.3

4,031 407 649 421 325 5,833

100.0

1 Gross impaired loans by industry sector as a percentage of total gross impaired loans.

Interest forgone on impaired loans

(Audited)

Interest income that would have been recognised

under the original terms of impaired and restructured

loans amounted to approximately US$1.1 billion

in 2007 (2006: US$0.7 billion). Interest income from

such loans of approximately US$374 million was

recorded in 2007.

Renegotiated loans

(Audited)

Restructuring activity is designed to manage

customer relationships, maximise collection

opportunities and, if possible, avoid foreclosure or

repossession. Such activities include extended

payment arrangements, approved external debt

management plans, deferring foreclosure,

modification, loan rewrites and/or deferral of

payments pending a change in circumstances.

Following restructuring, an overdue consumer

account is normally reset from delinquent to current

status. Restructuring policies and practices are based

on indicators or criteria which, in the judgement of

local management, indicate that repayment will

probably continue. These policies are required to be

kept under continual review and their application

varies according to the nature of the market, the