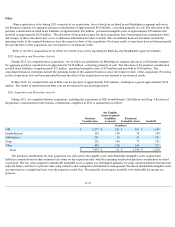

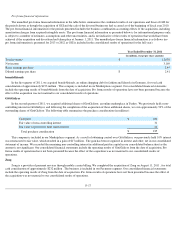

eBay 2013 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2013 eBay annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

|

|

eBay Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

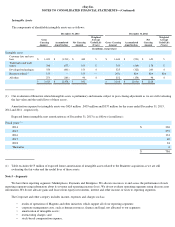

Loans and interest receivable, net

Loans and interest receivable represent purchased consumer receivables arising from loans made by a partner chartered financial institution

to individual consumers in the U.S. to purchase goods and services through our Bill Me Later merchant network. The terms of the consumer

relationship require us to submit monthly bills to the consumer detailing loan repayment requirements. The terms also allow us to charge the

consumer interest and fees in certain circumstances. Due to the relatively small dollar amount of individual loans and interest receivable, we do

not require collateral on these balances.

As part of the arrangement with the partner chartered financial institution in 2013, we sell a participation interest in the entire pool of

consumer receivables outstanding to the same financial institution. We apply a control-oriented, financial-

components approach and account for

the asset transfer as a sale and derecognize the portion of participation interest for which control has been surrendered. We do not recognize any

gains or losses on the sale of the participating interest as the carrying amount of the participating interest sold approximates the fair value at time

of transfer. Participating interest that is retained are included in loans and interest receivable and are accounted for at amortized cost, net of an

allowance for loan losses. We maintain the servicing rights for the entire pool of consumer receivables outstanding and receive a fee

approximating fair value for servicing the assets underlying the participating interest sold.

Allowance for loans and interest receivable

The allowance for loans and interest receivable represents management's estimate of probable losses inherent in our Bill Me Later portfolio

of loan receivables. The provision related to the principal is included in provision for transaction and loan losses and the provision related to the

interest is recorded as a reduction of marketing services and other revenue. The allowance includes probable losses which are considered to be of

one segment and one class. Management's evaluation of probable losses is subject to judgments and numerous estimates, including forecasted

principal balance delinquency rates ("roll rates"). Roll rates are the percentage of balances that we estimate will migrate from one stage of

delinquency to the next based on our historical experience, as well as external factors such as estimated bankruptcies and levels of

unemployment. The roll rates are applied to principal and interest balances for each stage of delinquency, from current to 180 days past due, in

order to estimate the loans and interest receivable that are probable to be charged off by the end of 180 days.

We charge off loans and interest receivable in the month in which the customer balance becomes 180 days past due. Bankrupt accounts are

charged off within 60

days of receiving notification of customer bankruptcy from the courts. Past due loans receivable continue to accrue interest

until such time as they are charged-off.

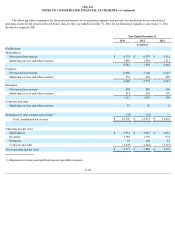

Funds receivable and funds payable

Funds receivable and funds payable relate primarily to our Payments segment and arise due to the time to clear transactions through

external payment networks. When customers fund their account using their bank account or credit card, or withdraw money to their bank account

or through a debit card transaction, there is a clearing period before the cash is received or settled, usually one to three business days for

U.S. transactions, and generally up to five business days for international transactions.

Customer accounts and amounts due to customers

Customer accounts and amounts due to customers relate primarily to our Payments segment and based on differences in regulatory

requirements and commercial law in the jurisdictions where PayPal operates, PayPal holds customer balances either as direct claims against

PayPal or as an agent or custodian on behalf of PayPal's customers. Customer balances held by PayPal as an agent or custodian on behalf of its

customers are not reflected on our consolidated balance sheet, while customer balances held as direct claims against PayPal are reflected on our

consolidated balance sheet as a liability classified as amounts due to customers. At December 31, 2012 and 2013, PayPal held all customer

balances (both in the U.S. and internationally) as direct claims against PayPal. Further, various jurisdictions where PayPal operates requires us to

hold eligible liquid assets, as defined by the regulators in these jurisdictions, equal to at least 100% of the aggregate amount of all customer

balances. Therefore, we use the assets underlying the customer balances to meet these regulatory requirements and separately classify the assets

as customer accounts in our consolidated balance sheets. We do not commingle the assets underlying the customer balances with corporate funds

and separately maintain these assets in interest and non-interest bearing bank deposits, time deposits and government and agency securities with

maturity dates of less than one year.

F-11