LeapFrog 2002 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2002 LeapFrog annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

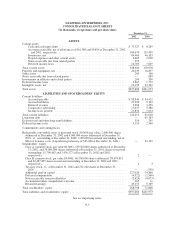

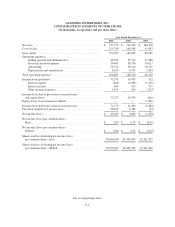

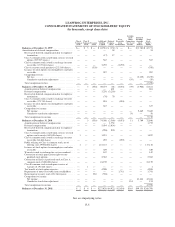

LEAPFROG ENTERPRISES, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(In thousands, except share, per share and percent data)

fiscal years ending after December 15, 2002. The disclosure provisions of this statement have been included in

the Company’s 2002 financial statements.

In November 2002, the FASB issued Interpretation No. 45, Guarantor’s Accounting and Disclosure

Requirement for Guarantees, Including Indirect Guarantees of Indebtedness of Others, (“FIN 45”). FIN 45

elaborates on the existing disclosure requirements for most guarantees, including residual value guarantees issued

in conjunction with operating lease agreements. It also clarifies that at the time a company issues a guarantee, the

company must recognize an initial liability for the fair value of the obligation it assumes under that guarantee and

must disclose that information in its interim and annual financial statements. The initial recognition and

measurement provisions apply on a prospective basis to guarantees issued or modified after December 31, 2002.

The disclosure requirements are effective for financial statements of interim or annual periods ending after

December 15, 2002. The adoption of FIN 45 did not have a material impact on the Company’s results of

operations or financial position.

In January 2003, the FASB issued Interpretation No. 46, Consolidation of Variable Interest Entities (“FIN

46”). The objective of FIN 46 is to improve financial reporting by companies involved with variable interest

entities by requiring the variable interest entity to be consolidated by a company if that company is subject to a

majority of the risk of loss from the variable interest entity’s activities or entitled to receive a majority of the

entity’s residual returns or both. Variable interests held in the same entity by a related party will be treated as the

company’s own interest in the determination of when consolidation is required. The consolidation requirements

of FIN 46 apply immediately to variable interest entities created after January 31, 2003. The consolidation

requirements apply to older entities in the first fiscal year or interim period beginning after June 15, 2003. The

Company is currently evaluating the provisions of FIN 46 and will adopt this Interpretation in the first quarter of

fiscal year 2003.

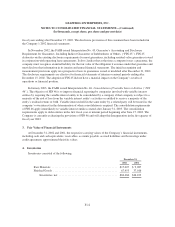

3. Fair Value of Financial Instruments

At December 31, 2002 and 2001, the respective carrying values of the Company’s financial instruments,

including cash and cash equivalents, receivables, accounts payable, accrued liabilities and borrowings under

credit agreement, approximated their fair values.

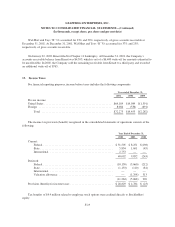

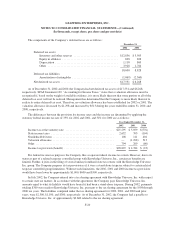

4. Inventories

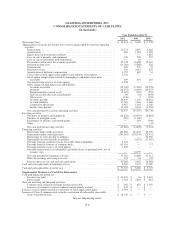

Inventories consisted of the following:

December 31,

2002 2001

Raw Materials .............................................. $17,007 $ 9,087

Finished Goods ............................................. 67,453 37,016

Inventories, net ......................................... $84,460 $46,103

F-12