Medtronic 2008 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2008 Medtronic annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

or (iii) there is an expiration of the statute of limitations. Significant

judgment is required in accounting for tax reserves. Although we

believe that we have adequately provided for liabilities resulting from

tax assessments by taxing authorities, positions taken by these tax

authorities could have a material impact on our effective tax rate in

future periods.

In the event there is a special, restructuring, certain litigation and/or

IPR&D charge recognized in our operating results, the tax cost or benefit

attributable to that item is separately calculated and recorded. Because

the effective rate can be significantly impacted by these discrete items

that take place in the period, we often refer to our tax rate using both

the effective rate and the non-GAAP nominal tax rate. The non-GAAP

nominal tax rate is defined as the income tax provision as a percentage

of taxable income, excluding special, restructuring, certain litigation and

IPR&D charges. We believe that this resulting non-GAAP financial

measure provides useful information to investors because it excludes

the effect of these discrete items so that investors can compare our

recurring results over multiple periods.

Tax regulations require certain items to be included in the tax return

at different times than when those items are required to be recorded

in the consolidated financial statements. As a result, our effective tax

rate reflected in our consolidated financial statements is different than

that reported in our tax returns. Some of these differences are

permanent, such as expenses that are not deductible on our tax return,

and some are temporary differences, such as depreciation expense.

Temporary differences create deferred tax assets and liabilities. Deferred

tax assets generally represent items that can be used as a tax deduction

or credit in our tax return in future years for which we have already

recorded the tax benefit in our consolidated statements of earnings. We

establish valuation allowances for our deferred tax assets when the

amount of expected future taxable income is not likely to support the

use of the deduction or credit. Deferred tax liabilities generally represent

tax expense recognized in our consolidated financial statements for

which payment has been deferred or expense has already been taken

as a deduction on our tax return but has not yet been recognized as an

expense in our consolidated statements of earnings.

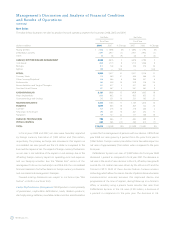

The Company’s overall tax rate including the tax impact on special,

restructuring, certain litigation and IPR&D charges has resulted in an

effective tax rate of 22.7 percent for fiscal year 2008. Excluding the

impact of these items, our operational and tax strategies have resulted

in a non-GAAP nominal tax rate of 21.0 percent versus the U.S. statutory

rate of 35.0 percent. An increase in our nominal tax rate of 1.0 percent

would result in an additional income tax provision for the fiscal year

ended April 25, 2008 of approximately $38 million. See discussion of the

tax rate in the “Income Taxes” section of the management’s discussion

and analysis.

Valuation of IPR&D, Goodwill and Other Intangible Assets When we

acquire a company, the purchase price is allocated, as applicable,

between IPR&D, other identifiable intangible assets, net tangible assets

and goodwill as required by U.S. GAAP. IPR&D is defined as the value

assigned to those projects for which the related products have not

received regulatory approval and have no alternative future use.

Determining the portion of the purchase price allocated to IPR&D and

other intangible assets requires us to make significant estimates. The

amount of the purchase price allocated to IPR&D and other intangible

assets is determined by estimating the future cash flows of each project

or technology and discounting the net cash flows back to their present

values. The discount rate used is determined at the time of acquisition

in accordance with accepted valuation methods. For IPR&D, these

methodologies include consideration of the risk of the project not

achieving commercial feasibility.

Goodwill represents the excess of the aggregate purchase price over

the fair value of net assets, including IPR&D, of the acquired businesses.

Goodwill is tested for impairment annually, or more frequently if

changes in circumstances or the occurrence of events suggest that the

carrying amount may be impaired.

The test for impairment requires us to make several estimates about

fair value, most of which are based on projected future cash flows.

Our estimates associated with the goodwill impairment tests are

considered critical due to the amount of goodwill recorded on

our consolidated balance sheets and the judgment required in

determining fair value amounts, including projected future cash flows.

Goodwill was $7.519 billion and $4.327 billion as of April 25, 2008 and

April 27, 2007, respectively.

Other intangible assets consist primarily of purchased technology,

patents and trademarks and are amortized using the straight-line or

accelerated method, as appropriate, over their estimated useful lives,

ranging from 3 to 20 years. As of April 25, 2008, all of our intangible

assets are definite lived and amortized on a straight-line basis. We

review these intangible assets for impairment annually or as changes

in circumstance or the occurrence of events suggest the remaining

value may not be recoverable. Other intangible assets, net of

accumulated amortization, were $2.193 billion and $1.433 billion as of

April 25, 2008 and April 27, 2007, respectively.

21Medtronic, Inc.