AT&T Wireless 2011 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2011 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

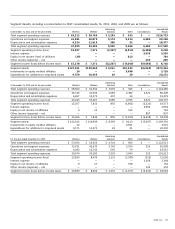

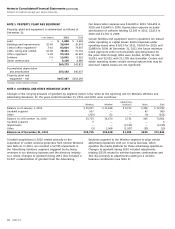

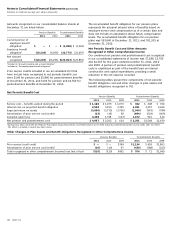

Notes to Consolidated Financial Statements (continued)

Dollars in millions except per share amounts

74 AT&T Inc.

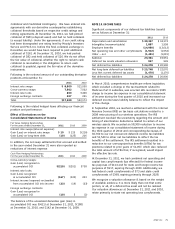

We designate our cross-currency swaps as cash flow hedges.

We have entered into multiple cross-currency swaps to hedge

our exposure to variability in expected future cash flows that

are attributable to foreign currency risk generated from the

issuance of our Euro and British pound sterling denominated

debt. These agreements include initial and final exchanges

of principal from fixed foreign denominations to fixed U.S.

denominated amounts, to be exchanged at a specified rate,

which was determined by the market spot rate upon issuance.

They also include an interest rate swap of a fixed foreign-

denominated rate to a fixed U.S. denominated interest rate.

We evaluate the effectiveness of our cross-currency swaps

each quarter. In the years ended December 31, 2011, and

December 31, 2010, no ineffectiveness was measured.

Periodically, we enter into and designate interest rate locks

to partially hedge the risk of changes in interest payments

attributable to increases in the benchmark interest rate during

the period leading up to the probable issuance of fixed-rate

debt. We designate our interest rate locks as cash flow

hedges. Gains and losses when we settle our interest rate

locks are amortized into income over the life of the related

debt, except where a material amount is deemed to be

ineffective, which would be immediately reclassified to

income. In the years ended December 31, 2011, and

December 31, 2010, no ineffectiveness was measured.

Over the next 12 months, we expect to reclassify $28 from

accumulated OCI to interest expense due to the amortization

of net losses on historical interest rate locks. Our unutilized

interest rate locks carry mandatory early terminations, the

latest occurring in April 2012. In April 2011, we utilized

$2,600 notional value of interest rate locks related to our

April 2011 debt issuance. In February 2012, we utilized

$800 notional value of interest rate locks related to our

February 2012 debt issuance (see Note 8). Over the next

12 months, we expect to reclassify an additional $15 from

accumulated OCI to interest expense due to the amortization

of net losses on the interest rate locks associated with this

debt issuance.

We hedge a large portion of the exchange risk involved in

anticipation of highly probable foreign currency-denominated

transactions. In anticipation of these transactions, we often

enter into foreign exchange contracts to provide currency at a

fixed rate. Some of these instruments are designated as cash

flow hedges while others remain nondesignated, largely based

on size and duration. Gains and losses at the time we settle

or take delivery on our designated foreign exchange contracts

are amortized into income in the same period the hedged

transaction affects earnings, except where an amount is

deemed to be ineffective, which would be immediately

reclassified to income. In the years ended December 31, 2011,

and December 31, 2010, no ineffectiveness was measured.

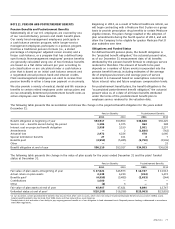

Derivative Financial Instruments

We employ derivatives to manage certain market risks,

primarily interest rate risk and foreign currency exchange

risk. This includes the use of interest rate swaps, interest

rate locks, foreign exchange forward contracts and

combined interest rate foreign exchange contracts (cross-

currency swaps). We do not use derivatives for trading

or speculative purposes. We record derivatives on our

consolidated balance sheets at fair value that is derived

from observable market data, including yield curves and

foreign exchange rates (all of our derivatives are Level 2).

Cash flows associated with derivative instruments are

presented in the same category on the consolidated

statements of cash flows as the item being hedged.

The majority of our derivatives are designated either as a

hedge of the fair value of a recognized asset or liability or

of an unrecognized firm commitment (fair value hedge), or

as a hedge of a forecasted transaction or of the variability

of cash flows to be received or paid related to a recognized

asset or liability (cash flow hedge).

Fair Value Hedging We designate our fixed-to-floating

interest rate swaps as fair value hedges. The purpose of these

swaps is to manage interest rate risk by managing our mix

of fixed-rate and floating-rate debt. These swaps involve

the receipt of fixed-rate amounts for floating interest rate

payments over the life of the swaps without exchange of the

underlying principal amount. Accrued and realized gains or

losses from interest rate swaps impact interest expense on

the consolidated statements of income. Unrealized gains on

interest rate swaps are recorded at fair market value as assets,

and unrealized losses on interest rate swaps are recorded at

fair market value as liabilities. Changes in the fair value of

the interest rate swaps offset changes in the fair value of

the fixed-rate notes payable they hedge due to changes in

the designated benchmark interest rate and are recognized

in interest expense. Gains or losses realized upon early

termination of our fair value hedges are recognized in interest

expense. In the years ended December 31, 2011, and

December 31, 2010, no ineffectiveness was measured.

Cash Flow Hedging Unrealized gains on derivatives

designated as cash flow hedges are recorded at fair value as

assets, and unrealized losses on derivatives designated as

cash flow hedges are recorded at fair value as liabilities, both

for the period they are outstanding. For derivative instruments

designated as cash flow hedges, the effective portion is

reported as a component of accumulated OCI until reclassified

into interest expense in the same period the hedged

transaction affects earnings. The gain or loss on the

ineffective portion is recognized as other income or

expense in each period.