Apple 1997 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 1997 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

|

|

TERMINATION OF LICENSE AGREEMENT

In August 1997, the Company agreed to acquire certain assets of Power Computing Corporation (PCC), a company which Apple had licensed

to distribute Macintosh operating systems. In addition to the acquisition of certain assets such as PCC's customer database and the license to

distribute Macintosh operating systems, the Company also has the right to retain certain key employees of PCC. The agreement with PCC also

includes a release of claims between the parties.

The Company anticipates it will complete its acquisition of the assets of PCC in the first quarter of 1998 once all regulatory approvals are

received. The total purchase price, which is comprised of shares of the Company's common stock valued at $100 million; the Company's

forgiveness of receivables from PCC; the assumption of certain PCC obligations; and closing and related costs, is expected to be approximately

$110 million. The total purchase price is expected to require total cash expenditures of approximately $5 million over the next 12 months. The

acquisition will be treated as a purchase for accounting purposes. The difference between the total purchase price and the amount expensed as

"Termination of License Agreement" on the accompanying consolidated statement of operations will be capitalized in the first quarter of 1998,

and then amortized over a period of two years.

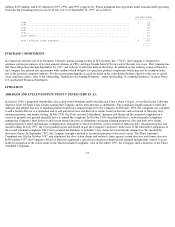

INCOME TAXES

The provision (benefit) for income taxes consists of the following:

The foreign provision (benefit) for income taxes is based on foreign pretax earnings (loss) of approximately $(265) million, $(141) million, and

$572 million in 1997, 1996, and 1995, respectively. A substantial portion of the Company's cash, cash equivalents, and short-term investments

is held by foreign subsidiaries and is generally based in U.S. dollar-denominated holdings. Amounts held by foreign subsidiaries would be

subject to U.S. income taxation on repatriation to the United States. The Company's consolidated financial statements fully provide for any

related tax liability on amounts that may be repatriated, aside from undistributed earnings of certain of the Company's foreign subsidiaries that

are intended to be indefinitely reinvested in operations outside the United States. U.S. income taxes have not been provided on a cumulative

total of $395 million of such earnings. It is not practicable to determine the income tax liability that might be incurred if these earnings were to

be distributed. Except for such

46

1997 1996 1995

--------- --------- ---------

(IN MILLIONS)

Federal:

Current............................................................. $ -- $ (125) $ 26

Deferred............................................................ -- (279) 113

--------- --------- ---------

-- (404) 139

--------- --------- ---------

State:

Current............................................................. -- (2) 1

Deferred............................................................ -- (71) 15

--------- --------- ---------

-- (73) 16

--------- --------- ---------

Foreign:

Current............................................................. -- (1) 89

Deferred............................................................ -- (1) 6

--------- --------- ---------

-- (2) 95

--------- --------- ---------

Provision (benefit) for income taxes.................................. $ -- $ (479) $ 250

--------- --------- ---------

--------- --------- ---------