Apple 2004 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2004 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

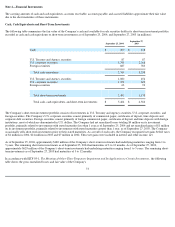

|

|

shipped and is being recognized on a straight-line basis in accordance with SFAS No. 86 over a 3 year estimated useful life. In addition, during

2002, the Company also began capitalizing certain costs related to development of its new PowerSchool enterprise student information system.

Capitalization of approximately $6 million began upon achievement of technological feasibility in the first quarter of 2002. The final version of

the enterprise student information system was released in July 2002.

Total amortization related to capitalized software development costs was $10.7 million, $5.8 million, and $1.2 million in 2004, 2003 and 2002,

respectively.

Advertising Costs

Advertising costs are expensed as incurred. Advertising expense was $206 million, $193 million, and $209 million for 2004, 2003, and 2002,

respectively.

Restructuring Charges

In June 2002, the FASB issued SFAS No. 146, Accounting for Costs Associated with Exit or Disposal Activities . SFAS No. 146 supersedes

Emerging Issues Task Force (EITF) Issue No. 94-3, Liability Recognition for Certain Employee Termination Benefits and Other Costs To Exit

an Activity (Including Certain Costs Associated with a Restructuring) and requires that a liability for a cost associated with an exit or disposal

activity be recognized when the liability is incurred, as opposed to when management commits to an exit plan. SFAS No. 146 also establishes

that the liability should initially be measured and recorded at fair value. This Statement was effective for exit or disposal activities initiated after

December 31, 2002. The provisions of SFAS No. 146 were required to be applied prospectively after the adoption date to newly initiated exit

activities.

Stock-Based Compensation

The Company measures compensation expense for its employee stock-based compensation plans using the intrinsic value method prescribed by

Accounting Principles Board (APB) Opinion No. 25, Accounting for Stock Issued to Employees. The Company applies the disclosure provisions

of SFAS No. 123, Accounting for Stock-based Compensation , as amended by SFAS No. 148 , Accounting for Stock-based Compensation—

Transition and Disclosure as if the fair value-based method had been applied in measuring compensation expense. The Company has elected to

follow APB Opinion No. 25 because, as discussed below, the alternative fair value accounting provided for under SFAS No. 123 requires use of

option valuation models that were not developed for use in valuing employee stock options and employee stock purchase plan shares. Under

APB Opinion No. 25, when the exercise price of the Company's employee stock options equals the market price of the underlying stock on the

date of the grant, no compensation expense is recognized.

As required under SFAS No. 123, the pro forma effects of stock-based compensation on net income and earnings per common share for

employee stock options granted and employee stock purchase plan share purchases have been estimated at the date of grant and beginning of the

period, respectively, using a Black-Scholes option pricing model. For purposes of pro forma disclosures, the estimated fair value of the options

and shares is amortized to pro forma net income (loss) over the options' vesting period and the shares' plan period.

The Black-Scholes option valuation model was developed for use in estimating the fair value of freely traded options that have no vesting

restrictions and are fully transferable. In addition, option valuation models require the input of highly subjective assumptions including the

expected life of options and the Company's expected stock price volatility. Because the Company's employee stock options and employee

70