Bank of America 1999 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 1999 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35

|

|

Ask most people what they want out of

their banking relationship, and they will

talk about choice, convenience, service

and flexibility — not technology.

Where do you want your bank to be?

At home, at work, in the grocery store, on

the beach, inside my PalmTM organizer or

my laptop. Wherever I am.

How do you want to interact with

your bank? By phone, online, in person,

at an ATM , through the mail.

What hours would you like your bank

to be open? 24-7. All the time.

The Internet — and, just as important,

the digital technology that makes the

Internet possible — is a tool that helps us

provide more of what our customers and

clients want. We are using the Internet to

give customers and clients more options

and better ones, not simply a new single-

channel banking service.

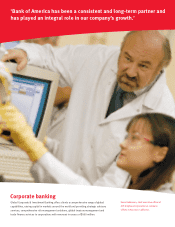

Today’s online consumer and small

business customers at Bank of America

will find industrial-strength capacity and

capabilities behind their computer screens.

This competence is the result of a

decade-long effort to build a flexible

infrastructure that provides consistent,

reliable information across a range of

convenient channels.

Today, our retail customers can apply

online for almost any banking product,

including checking and savings accounts,

CDs, IRAs, mortgages, credit or debit

cards, and auto loans. They can access

account information, transfer funds and

pay bills day or night.

Our customers also have online

access to Banc of America Investment

Services, which offers a broad spectrum of

investment products including stocks,

bonds and mutual funds. Our online

investment offering is supported by

research tools and resources that enable

customers to make informed investment

decisions, and also to integrate their

banking and investing activities. Today,

more than half of all our customers’self-

directed trades are conducted online.

Our leading small business Web site

enables our customers to set up their

own Internet storefront, establish online

payment methods, find low-cost sales

and marketing services, obtain good

deals on products and services, as well

as conduct their banking and apply for

credit online. With a small business

customer base of more than 1.7 million,

we expect to continue to be the leading

provider of online financial and business

services to American small business in

the future.

While our customers are rapidly

adopting the Internet as a channel for

doing business, most of them still value

the convenience of using multiple chan-

nels, including telephones, ATMs and

banking centers. That is why we are

in the process of wiring our delivery

channels with Internet protocols, which

will give customers access to the same

personalized, multi-product, service-rich

experience regardless of where they are.

For example, future Bank of America

customers will be able to make a request

— a copy of a check, perhaps, or notifi-

cation of a drop in mortgage interest

rates — and have that request fulfilled

across the spectrum of delivery channels

in real time. The next time the customer

logs on, calls in or visits an ATM or a

banking center, the fulfillment of the

request — the check image, the mortgage

e-everythi

24

Every month Bank of America adds

100,000 new online banking customers

and processes 2.6-million online bill

payments. We also are continuing

to expand Internet capabilities for

thousands of business and

corporate clients.