Bank of America 1999 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 1999 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

|

|

This is not a product strategy, a single business line strategy or a channel

strategy. It is a customer-focused relationship strategy that will guide our entire

company in all we do.

You can read more about how this strategy is being brought to life for each of

our primary customer and client groups later in this report. But, the bottom line

is this: We’ve spent the past 20 years building the largest footprint, the strongest

market share and the best customer and client base in America. Our job now is to

give 30 million customer households and 2 million business clients good reasons to

bring us more of their business.

By integrating our businesses, we will take the burden of aggregating our

products and services off our customers’ and clients’ backs and put it back where

it belongs: on our own. For years, banks have asked customers for more of their

business. Customers, however, have been required to do the hard work of obtaining

and managing each product or service separately.

We’ve been working to integrate our businesses for our commercial and

corporate clients over the past five years by appointing client managers to

coordinate the delivery of multiple products and services to individual clients.

Today, networking technology is enabling us to aggregate information for clients

and associates by building bridges within our infrastructure, making it easier to

understand and manage the full breadth of our relationships.

This same networking technology also will enable our retail and small business

customers to manage their relationships with us as one company. Personal bankers

and small business bankers, too, are gaining the ability to work with customers

within the context of the customer’s full relationship with the bank.

Integration of our businesses makes the second point in our strategy possible:

rewarding customers and clients for doing more business with us. This part of our

strategy may take many forms, from package pricing to enhanced service options to

simply letting customers know that we appreciate their decision to give us their

business. The point is, if we’re asking customers and clients to bring us more of

their business, we should be willing to reward them when they do.

The third part of our strategy is about setting priorities. In a fast-changing

competitive environment, we have to look hard and often at how we are deploying

our resources. We are ensuring that the businesses, products and projects in which

we are investing make sense within the context of our relationship strategy and are

creating value for customers, clients and shareholders. Making tough decisions

based on these criteria will bring focus and vigor to our efforts across the company.

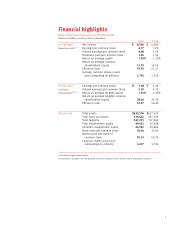

Strong financial performance and new financial targets.

Looking at our business and financial accomplishments in 1999, the year was

something of an enigma. We produced a significant increase in earnings, fulfilling

the guidance we provided Wall Street in January, and continued to make good

progress on our merger transition and business strategy. Yet, our stock went down.

In 1999, your company had operating earnings of $8.2 billion, a 27 percent

increase over 1998, on record revenues of $32.5 billion. We achieved this improvement

through favorable operating leverage. That is, we increased revenues by 6 percent

through healthy advances in such fee-based businesses as investment banking,

deposit services, card services and mortgage banking. At the same time, we reduced

expenses by 4 percent, primarily as a result of our successful consolidation efforts

in the wake of recent mergers. Our credit losses declined by almost $500 million,

allowing us to lower provision expense.

4

96 97 98 99

1.37

1.20

1.59

1.85

96 97 98 99

14.5

15.9

17.0

17.7

Dividends

(Dollars per share)

Return on average

common equity

(operating basis)

(Percent)