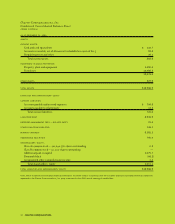

Charter 1999 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 1999 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

|

|

14 CHARTER COMMUNICATIONS

• the successful “Charterizing” of recently acquired cable systems, bringing these systems

up to Charter’s high standards of operational and financial performance;

• the rapid, effective deployment of new digital services in markets throughout our systems;

• a continued focus on improving service to our customers; and

• the continuation of strategic acquisitions and system swaps to improve clustering of our systems.

I firmly believe that we’ll end 2000 ahead of our original schedule for rebuilding our systems

without increasing our overall cost projections. Our plant architecture is state-of-the-art. Our

current design standards include six fiber-optic strands to each node serving a maximum of 500

homes, and currently averaging 380 homes per node. By activating the fibers reserved for future use,

utilizing dense wavelength division multiplexing, we can segment to 60 home nodes. This positions

us very well to achieve high penetration levels for all of our advanced services.

Our plans call for adding an average of 10,000 new digital video customers and 2,500 new

high-speed Internet service customers a week in 2000. We also plan to offer our Internet

portal service in St. Louis and other select markets in 2000, and to move ahead with trials of video

on demand and telephone service.

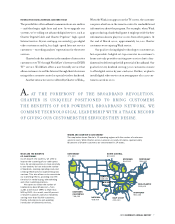

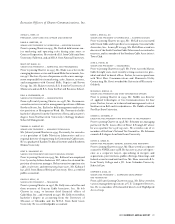

STRONG MARKETS NUMBER OF CUSTOMERS

Los Angeles, Calif. 509,000

Greenville/Spartanburg, S.C. 321,000

St. Louis, Mo. 255,000

Madison, Wisc. 231,000

Atlanta, Ga. 210,000

Charleston, W. Va. 189,000

Ft. Worth, Texas 188,000

Worchester, Mass. 165,000

Rochester, Minn. 142,000

Bay City, Mich. 132,000

Kingsport, Tenn. 124,000

Hickory, N.C. 122,000

Birmingham, Ala. 117,000

Fond du Lac, Wisc. 107,000

Charter’s acquisition strategy has resulted in significant progress in

clustering our cable operations. Approximately 45 percent of Charter

customers are in 14 markets with an average of 200,000 customers

each, and 80 percent of all Charter customers are in 14 states.

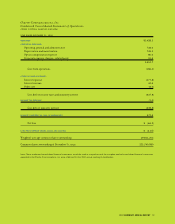

96 97 98 99

9.6

9.5

10.7

9.1

96 97 98 99

10.0

11.0

11.4

10.6

Over the past four years, Charter has maintained consistently strong

growth in both “same-store” (for systems under Charter management

for 12 months or more) revenues and EBITDA — earnings before inter-

est, income taxes, depreciation and amortization.

CONSISTENTLY STRONG PERFORMANCE

“SAME-STORE” REVENUE GROWTH “SAME-STORE” EBITDA GROWTH

in percent in percent