GE 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

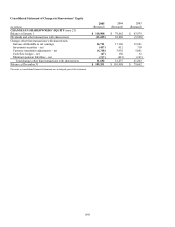

|

|

(61)

PENSION ASSUMPTIONS are significant inputs to the actuarial models that measure pension benefit obligations

and related effects on operations. Two assumptions-discount rate and expected return on assets-are important

elements of plan expense and asset/liability measurement. We evaluate these critical assumptions at least annually

on a plan and country-specific basis. We evaluate other assumptions involving demographic factors such as

retirement age, mortality and turnover periodically and update them to reflect our experience and expectations for

the future. Actual results in any given year will often differ from actuarial assumptions because of economic and

other factors.

Accumulated and projected benefit obligations are expressed as the present value of future cash payments.

We discount those cash payments using the weighted average of market-observed yields for high quality fixed

income securities with maturities that correspond to the payment of benefits. Lower discount rates increase present

values and subsequent year pension expense; higher discount rates decrease present values and subsequent year

pension expense.

To reflect market interest rate conditions, we reduced our discount rate for principal pension plans at

December 31, 2005, from 5.75% to 5.50% and at December 31, 2004, from 6.0% to 5.75%.

To determine the expected long-term rate of return on pension plan assets, we consider the current and

expected asset allocations, as well as historical and expected returns on various categories of plan assets. Assets in

our principal pension plans earned 10.2% in 2005 and had average annual earnings of 4.7%, 10.1% and 11.8% per

year in the five, 10 and 25-year periods ended December 31, 2005, respectively. We believe that these results, in

connection with our current and expected asset allocations, support our assumed long-term return of 8.5% on those

assets.

Sensitivity to changes in key assumptions for our principal pension plans follows.

• Discount rate-A 25 basis point reduction in discount rate would increase pension cost in the following year by

$0.2 billion.

• Expected return on assets-A 50 basis point increase in the expected return on assets would decrease pension

cost in the following year by $0.2 billion.

Further information on our pension plans is provided in the Operations-Overview section and in note 7.

DERIVATIVES AND HEDGING. We use derivatives to manage a variety of risks, including risks related to

interest rates, foreign exchange and commodity prices. Accounting for derivatives as hedges requires that, at

inception and over the term of the arrangement, the hedged item and related derivative meet the requirements for

hedge accounting. The accounting guidance related to derivatives accounting is complex. Failure to apply this

complex guidance correctly will result in all changes in the fair value of the derivative being reported in earnings,

while offsetting changes in the fair value of the hedged item are reported in earnings only upon realization,

regardless of whether the hedging relationship is economically effective.