HP 2006 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2006 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

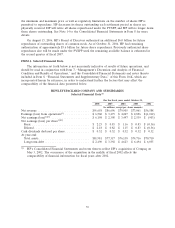

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

The following discussion should be read in conjunction with the Consolidated Financial Statements

and the related notes that appear elsewhere in this document.

OVERVIEW

We are a leading global technology company and generate net revenue and earn our profits from

the sale of products, technologies, solutions and services to consumers, businesses and governments.

Our portfolio is broad and includes personal computers, handheld computing devices, home and

business imaging and printing devices, publishing systems, storage and servers, a wide array of

information technology (‘‘IT’’) services and software solutions. We have seven business segments:

Enterprise Storage and Servers (‘‘ESS’’), HP Services (‘‘HPS’’), Software, the Personal Systems Group

(‘‘PSG’’), the Imaging and Printing Group (‘‘IPG’’), HP Financial Services (‘‘HPFS’’), and Corporate

Investments. ESS, HPS and Software are structured beneath a broader Technology Solutions Group

(‘‘TSG’’). While TSG is not an operating segment, we sometimes provide financial data aggregating the

segments within TSG in order to provide a supplementary view of our business.

Our product and geographic breadth requires us to focus on strategic imperatives within individual

product categories and to manage across our portfolio in order to drive growth while optimizing cost

structure. Our financial results also are impacted by our ability to predict and to respond to

industry-wide trends. For instance, a trend that is significant to our business and financial results is the

shift toward standardized products, which presents revenue opportunities for certain of our businesses

but presents an ongoing challenge to our margins. To help address the potential margin impact of

standardization, we take ongoing actions related to both revenue generation and cost structure

management. In the sales and marketing area, we have programs designed to improve the rates at

which we sell higher-margin configurations or options. We also continue to focus on managing

procurement and labor expenses. Key to our overall efforts in delivering superior products while

maintaining a world-class cost structure is the increasingly global nature of technology expertise. This

trend is allowing us to develop a global delivery structure to take advantage of regions where advanced

technical expertise is available at lower costs.

As part of our efforts to improve efficiencies and reduce costs, we continually evaluate our

workforce and infrastructure and make adjustments we deem appropriate. When we make adjustments

to our workforce and infrastructure, we may incur incremental expenses that delay the benefit of a

more efficient workforce structure, but we believe that the fundamental shift to more efficient global

delivery is crucial to maintaining a long-term competitive cost structure. Recent adjustments include:

• Our plans announced in May 2006 to reduce our IT spending by consolidating 85 data centers

worldwide into six state-of-the-art centers in three U.S. cities; and

• Our plans announced in July 2006 to reduce our real estate costs by consolidating several

hundred real estate locations worldwide to fewer core sites over the next four years.

We continue to implement the 2005 restructuring plan that was approved by our Board of

Directors in the fourth quarter of fiscal 2005. As part of that plan, we announced in June 2006 that we

would integrate the activities carried out by our Global Operations organization directly into our

business segments. Under the 2005 restructuring plan, we expect to eliminate approximately 15,200

positions through workforce restructuring or early retirement programs. Approximately 14,200 of these

positions have been eliminated as of October 31, 2006. The majority of the remaining 1,000 positions

35