Starbucks 2001 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2001 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

adopted Issue No. 00-10 on October 2, 2000, and restated all prior period disclosures. Issue No. 00-

10 did not have a material impact on the Company’s consolidated financial statements.

In July 2001, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial

Accounting Standards (“SFAS”) No. 141,“Business Combinations,” and SFAS No. 142,“Goodwill and

Other Intangible Assets.” SFAS No. 141 requires the use of the purchase method of accounting for

business combinations initiated after June 30,2001,and eliminates the pooling-of-interests method.SFAS

No. 142 requires, among other things, the use of a nonamortization approach for purchased goodwill

and certain intangibles. Under a nonamortization approach, goodwill and certain intangibles will not be

amortized into earnings, but instead will be reviewed for impairment at least annually.The Company

will adopt SFAS No. 142 effective September 30, 2002. The Company’s management has not yet

determined the impact of adoption on its consolidated financial position and results of operations.As of

September 30, 2001, the Company had goodwill and other intangible assets, net of accumulated

amortization, of $21.8 million and $7.7 million, respectively, which would be subject to the transitional

assessment provisions of SFAS No. 142.Amortization expense related to goodwill and other intangible

assets was $3.0 million for the fiscal year ended September 30, 2001.

In June 2001, the FASB issued SFAS No. 143,“Accounting for Asset Retirement Obligations.” SFAS

No. 143 requires that the fair value of a liability for an asset retirement obligation be recognized in

the period in which it is incurred if a reasonable estimate of fair value can be made.The associated

asset retirement costs are capitalized as part of the carrying amount of the long-lived asset. The

Company will adopt SFAS No. 143 effective September 30, 2002, and does not expect it to have a

material impact on the Company’s consolidated results of operations, financial position or cash flows.

In August 2001,the FASB issued SFAS No.144,“Accounting for the Impairment or Disposal of Long-

Lived Assets,” which supercedes SFAS No.121,“Accounting for the Impairment of Long-Lived Assets

and for Long-Lived Assets to Be Disposed Of.” SFAS No. 144 retains the fundamental provisions of

SFAS No. 121 but sets forth new criteria for asset classification and broadens the scope of qualifying

discontinued operations. The Company will adopt SFAS No. 144 as of September 30, 2002. The

Company’s management has not yet determined the impact of adoption on its consolidated financial

position and results of operations.

In September 2001, the EITF reached a consensus regarding Issue No. 01-10,“Accounting for the

Impact of the Terrorist Attacks of September 11, 2001,” which requires that losses and other costs

incurred as a result of the September 11, 2001, events be classified as part of income from continuing

operations in the statement of operations. Additionally, certain disclosures are required in all periods

affected. As a result of the events of September 11, 2001, the Company closed its North American

Company-operated retail stores and other North American facilities for the remainder of that day.

None of the Company’s employees were injured,and the Company did not sustain significant property

loss or incur significant costs as a result of the attacks. However, the aftermath of these events, together

with the slowing economy, have had a moderately negative impact on the Company’s Specialty

Operations,which derives approximately 9.0% of its revenue from the travel and hospitality industries.

At this time, management believes that the events of September 11, 2001, will not have a material

impact on the Company’s financial position, results of operations or cash flows in fiscal 2002.

Subsequent Events

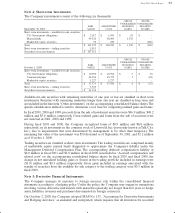

On October 10, 2001, the Company sold 30,000 of its shares of Starbucks Coffee Japan, Ltd.

(“Starbucks Japan”) at approximately $495.00 per share, net of related costs. In connection with this

sale, the Company received cash proceeds of $15 million. The Company’s ownership interest in

Starbucks Japan was reduced from 50.0% to 47.5% following the sale of the aforementioned shares.

The Company recorded a gain from this sale of $13 million.

Also on October 10, 2001, Starbucks Japan issued and sold 220,000 shares of common stock at

approximately $495.00 per share, net of related costs, in an initial public offering in Japan. In

connection with this offering, the Company’s ownership interest in Starbucks Japan was reduced from

47.5% to 40.1%.The Company recorded a credit to shareholders’equity of $39 million, reflecting the

increase in value of its share of the net assets of Starbucks Japan related to the stock offering.