Starbucks 2001 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2001 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

|

|

Fiscal 2001 Annual Report 35

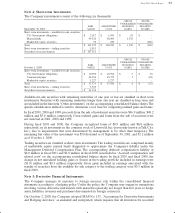

expenses,” on the accompanying consolidated statements of earnings were $28.8 million,$32.6 million

and $38.4 million in 2001, 2000 and 1999, respectively.

STORE PREOPENING EXPENSES

Costs incurred in connection with the start-up and promotion of new store openings are expensed as

incurred.

RENT EXPENSE

Certain of the Company’s lease agreements provide for scheduled rent increases during the lease terms

or for rental payments commencing at a date other than the date of initial occupancy. Minimum rental

expenses are recognized on a straight-line basis over the terms of the leases.

FOREIGN CURRENCY TRANSLATION

The Company’s international operations use their local currency as their functional currency.Assets

and liabilities are translated at exchange rates in effect at the balance sheet date. Income and expense

accounts are translated at the average monthly exchange rates during the year. Resulting translation

adjustments are recorded as a separate component of accumulated other comprehensive income.

INCOME TAXES

The Company computes income taxes using the asset and liability method, under which deferred

income taxes are provided for the temporary differences between the financial reporting basis and the

tax basis of the Company’s assets and liabilities.

STOCK SPLIT

On April 27, 2001, the Company effected a two-for-one stock split of its $0.001 par value common

stock for holders of record on March 30, 2001. All applicable share and per-share data in these

consolidated financial statements have been restated to give effect to this stock split.

EARNINGS PER SHARE

The computation of basic earnings per share is based on the weighted average number of shares and

common stock units outstanding during the period.The computation of diluted earnings per share

includes the dilutive effect of common stock equivalents consisting of certain shares subject to stock

options.

RECENT ACCOUNTING PRONOUNCEMENTS

In September 2000, the Emerging Issues Task Force (“EITF”) reached a consensus regarding Issue No.

00-10, “Accounting for Shipping and Handling Fees and Costs,” which requires any shipping and

handling costs billed to customers in a sale transaction to be classified as revenue. The Company

adopted Issue No. 00-10 on October 2, 2000, and restated all prior period disclosures. Issue No. 00-

10 did not have a material impact on the Company’s consolidated financial statements.

In July 2001, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial

Accounting Standards (“SFAS”) No. 141,“Business Combinations,” and SFAS No. 142,“Goodwill and

Other Intangible Assets.” SFAS No. 141 requires the use of the purchase method of accounting for

business combinations initiated after June 30,2001,and eliminates the pooling-of-interests method.SFAS

No. 142 requires, among other things, the use of a nonamortization approach for purchased goodwill

and certain intangibles. Under a nonamortization approach, goodwill and certain intangibles will not be

amortized into earnings, but instead will be reviewed for impairment at least annually.The Company

will adopt SFAS No. 142 effective September 30, 2002. The Company’s management has not yet

determined the impact of adoption on its consolidated financial position and results of operations.As of

September 30, 2001, the Company had goodwill and other intangible assets, net of accumulated

amortization, of $21.8 million and $7.7 million, respectively, which would be subject to the transitional

assessment provisions of SFAS No. 142.Amortization expense related to goodwill and other intangible

assets was $3.0 million for the fiscal year ended September 30, 2001.

In June 2001, the FASB issued SFAS No. 143,“Accounting for Asset Retirement Obligations.” SFAS

No. 143 requires that the fair value of a liability for an asset retirement obligation be recognized in

the period in which it is incurred if a reasonable estimate of fair value can be made.The associated

asset retirement costs are capitalized as part of the carrying amount of the long-lived asset. The

Company will adopt SFAS No. 143 effective September 30, 2002, and does not expect it to have a

material impact on the Company’s consolidated results of operations, financial position or cash flows.