Walgreens 2007 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2007 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

|

|

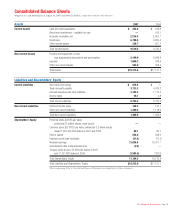

Notes to Consolidated Financial Statements

1. Summary of Major Accounting Policies

Description of Business

The company is principally in the retail drugstore business and its operations are

within one reportable segment. At August 31, 2007, there were 5,997 locations in

48 states and Puerto Rico. Prescription sales were 65.0% of total sales for fiscal

2007 compared to 64.3% in 2006 and 63.7% in 2005.

Basis of Presentation

The consolidated statements include the accounts of the company and its

subsidiaries. All intercompany transactions have been eliminated. The consolidated

financial statements are prepared in accordance with accounting principles

generally accepted in the United States of America and include amounts based

on management’s prudent judgments and estimates. Actual results may differ

from these estimates.

The balance sheet reflects the reclassification of goodwill from other non-current

assets. The cash flow statement contains reclassifications of previously condensed

lines within the operating activity section.

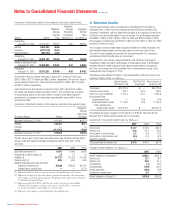

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand and all highly liquid investments

with an original maturity of three months or less. Included in cash and cash equiv-

alents are credit card and debit card receivables from banks, which generally settle

within two business days, of $67.0 million at August 31, 2007, and $54.7 million

at August 31, 2006. The company’s cash management policy provides for controlled

disbursement. As a result, the company had outstanding checks in excess of funds

on deposit at certain banks. These amounts, which were $302.6 million as of

August 31, 2007, and $575.3 million as of August 31, 2006, are included in trade

accounts payable in the accompanying consolidated balance sheets.

Short-Term Investments – Available for Sale

The company’s short-term investments – available for sale are principally auction

rate securities. The company invests in municipal bonds and student obligations

and purchases these securities at par. While the underlying security is issued as a

long-term investment, they typically can be purchased and sold every 7, 28 and 35

days. The trading of auction rate securities takes place through a descending price

auction with the interest rate reset at the beginning of each holding period. At the

end of each holding period the interest is paid to the investor. At August 31, 2007,

there were no holdings of auction rate securities compared to $415.1 million in

fiscal 2006. There were no significant unrealized gains on these securities at

August 31, 2006.

Financial Instruments

The company had $76.9 million and $105.1 million of outstanding letters of

credit at August 31, 2007 and 2006, respectively, which guarantee foreign trade

purchases. Additional outstanding letters of credit of $276.8 million and

$282.2 million at August 31, 2007 and 2006, respectively, guarantee payments

of casualty claims. The casualty claim letters of credit are annually renewable and

will remain in place until the casualty claims are paid in full. Letters of credit of

$12.2 million and $1.7 million were outstanding at August 31, 2007, and August

31, 2006, respectively, to guarantee performance of construction contracts. The

company pays a facility fee to the financing bank to keep these letters of credit

active. The company had real estate development purchase commitments of

$980.4 million and $782.8 million at August 31, 2007 and 2006, respectively.

There were no investments in derivative financial instruments during fiscal 2007

and 2006 except for the embedded derivative contained with the conversion

features of the $28.5 million of convertible debt acquired in the Option Care, Inc.

and affiliated companies acquisition. The value of such derivative is not material

and the debt was retired on September 6, 2007.

Inventories

Inventories are valued on a lower of last-in, first-out (LIFO) cost or market basis.

At August 31, 2007 and 2006, inventories would have been greater by

$968.8 million and $899.5 million, respectively, if they had been valued on a

lower of first-in, first-out (FIFO) cost or market basis. Inventory includes product

cost, inbound freight, warehousing costs and vendor allowances not included

as a reduction of advertising expense.

Cost of Sales

Cost of sales is derived based upon point-of-sale scanning information with an

estimate for shrinkage and is adjusted based on periodic inventories. In addition

to merchandise cost, cost of sales includes warehousing costs, purchasing costs,

freight costs, cash discounts and vendor allowances not included as a reduction

of advertising expense.

Vendor Allowances

Vendor allowances are principally received as a result of purchase levels, sales or

promotion of vendors’ products. Allowances are generally recorded as a reduction

of inventory and are recognized as a reduction of cost of sales when the related

merchandise is sold. Those allowances received for promoting vendors’ products

are offset against advertising expense and result in a reduction of selling, occupancy

and administration expenses to the extent of advertising costs incurred, with the

excess treated as a reduction of inventory costs.

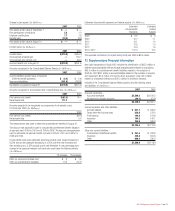

Property and Equipment

Depreciation is provided on a straight-line basis over the estimated useful lives of

owned assets. Leasehold improvements and leased properties under capital leases

are amortized over the estimated physical life of the property or over the term of

the lease, whichever is shorter. Estimated useful lives range from 121

/2to 39 years

for land improvements, buildings and building improvements and 3 to 121

/2years

for equipment. Major repairs, which extend the useful life of an asset, are capitalized

in the property and equipment accounts. Routine maintenance and repairs are

charged against earnings. The majority of the business uses the composite

method of depreciation for equipment; therefore, gains and losses on retirement

or other disposition of such assets are included in earnings only when an

operating location is closed, completely remodeled or impaired. Fully depreciated

property and equipment are removed from the cost and related accumulated

depreciation and amortization accounts. Property and equipment consists of

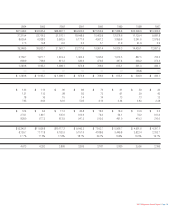

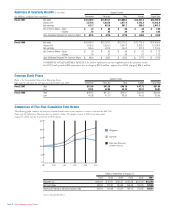

(In Millions):

2007 2006

Land and land improvements

Owned locations $ 2,011.8 $1,667.4

Distribution centers 102.7 94.2

Other locations 211.9 93.5

Buildings and building improvements

Owned locations 2,244.9 1,824.6

Leased locations (leasehold improvements only) 581.5 537.6

Distribution centers 553.2 483.4

Other locations 269.9 229.0

Equipment

Locations 3,604.2 3,157.7

Distribution centers 879.2 773.3

Other locations 266.0 214.4

Capitalized system development costs 207.9 171.7

Capital lease properties 43.3 40.2

10,976.5 9,287.0

Less: accumulated depreciation and amortization 2,776.6 2,338.1

$ 8,199.9 $6,948.9

2007 Walgreens Annual Report Page 27