Walgreens 2008 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2008 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

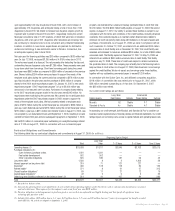

open approximately 540 new drugstores in fiscal 2009, with a net increase of

approximately 475 drugstores, and anticipate having a total of more than 7,000

drugstores by fiscal 2010. We intend to increase new drugstore organic growth by

6 percent and 5 percent in fiscal 2010 and 2011, respectively. During the current

fiscal year we added a total of 1,031 locations, of which 596 were new or relocated

drugstores, with a net gain of 561 drugstores after relocations and closings. We

are continuing to relocate stores to more convenient and profitable freestanding

locations. In addition to new stores, expenditures are planned for distribution

centers and technology. A new distribution center in Windsor, Connecticut, has

an anticipated opening date in fiscal 2009.

Net cash used for financing activities was $33 million compared to $626 million last

year. On July 17, 2008, we issued $1,300 million of 4.875% notes due in 2013.

The notes were issued at a discount. The net proceeds after deducting the discount,

underwriting fees and issuance costs were $1,286 million. These proceeds were used

to pay down short-term borrowings. Short-term borrowings paid during the current

fiscal year were $802 million as compared to $850 million of proceeds in the previous

year. Shares totaling $294 million were purchased to support the needs of the

employee stock plans during the current period as compared to $376 million a year

ago. Also included in the prior year was the purchase of $343 million of company

shares for the 2004 stock repurchase program. On January 10, 2007, a new stock

repurchase program (“2007 repurchase program”) of up to $1,000 million was

announced, to be executed over four years. Purchases of company shares relating

to the 2007 repurchase program made in the prior year were $345 million. No

repurchases were made during the current year. We currently do not anticipate stock

repurchases under the 2007 repurchase program in 2009, except to support the

needs of the employee stock plans. We had proceeds related to employee stock

plans of $210 million during the current fiscal year as compared to $266 million a

year ago. Cash dividends paid were $376 million during the current fiscal year versus

$310 million a year ago. A $214 million wire transfer made on August 31, 2006, was

not accepted by our disbursement bank until September 1, 2006, resulting in a bank

overdraft at fiscal 2006 year-end and subsequent repayment on September 1, 2006.

We had $70 million of commercial paper outstanding at a weighted-average interest

rate of 2.10% at August 31, 2008. In connection with our commercial paper

program, we maintained two unsecured backup syndicated lines of credit that total

$1,200 million. The first $600 million facility expires on August 10, 2009; the second

expires on August 12, 2012. Our ability to access these facilities is subject to our

compliance with the terms and conditions of the credit facilities, including financial

covenants. The covenants require us to maintain certain financial ratios related to

minimum net worth and priority debt, along with limitations on the sale of assets and

purchases of investments. As of August 31, 2008, we were in compliance with all

such covenants. On October 12, 2007, we entered into an additional $100 million

unsecured line of credit facility and on November 30, 2007, that credit facility was

amended and increased to include an additional $200 million, for a total of $300 million

unsecured credit. That facility expired on December 31, 2007. On May 15, 2008, we

entered into an additional $500 million unsecured line of credit facility. That facility

expired on July 31, 2008. These lines of credit were subject to similar covenants as

the syndicated lines of credit. The company pays a facility fee to the financing bank to

keep our lines of credit active. As of August 31, 2008, there have been no borrowings

against the credit facilities. We do not expect any borrowings under these facilities,

together with our outstanding commercial paper, to exceed $1,200 million.

In connection with the Option Care, Inc. and affiliated companies acquisition,

$118 million of convertible debt was retired prior to August 31, 2007, while

$28 million remained outstanding as of that date. On September 6, 2007,

the $28 million was retired.

Our current credit ratings are as follows:

Long-Term Commercial

Rating Agency Debt Rating Outlook Paper Rating Outlook

Moody’s A2 Stable P-1 Stable

Standard & Poor’s A+ Stable A-1 Stable

In assessing our credit strength, both Moody’s and Standard & Poor’s consider our

business model, capital structure, financial policies and financial statements. Our credit

ratings impact our borrowing costs, access to capital markets and operating lease costs.

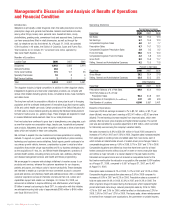

2008 Walgreens Annual Report Page 21

Contractual Obligations and Commitments

The following table lists our contractual obligations and commitments at August 31, 2008 (In millions):

Payments Due by Period

Less Than

Total 1 Year 1–3 Years 3–5 Years Over 5 Years

Operating leases (1) $33,038 $1,811 $3,849 $3,763 $23,615

Purchase obligations (2):

Open inventory purchase orders 1,931 1,931 — — —

Real estate development 952 952 — — —

Other corporate obligations 620 338 181 59 42

Long-term debt* 1,350 8 3 1,303 36

Interest payment on long-term debt 319 71 127 121 —

Insurance* 466 128 118 84 136

Retiree health* 371 8 21 27 315

Closed location obligations* 69 17 21 12 19

Capital lease obligations* 4225332

Other long-term liabilities reflected on the balance sheet* (3) 514 41 107 84 282

Total $39,672 $5,307 $4,432 $5,456 $24,477

* Recorded on balance sheet.

(1) Amounts for operating leases and capital leases do not include certain operating expenses under these leases such as common area maintenance, insurance

and real estate taxes. These expenses for the company’s most recent fiscal year were $298 million.

(2) Purchase obligations include agreements to purchase goods or services that are enforceable and legally binding and that specify all significant terms,

including open purchase orders.

(3) Includes $36 million ($19 million due in 1–3 years, $12 million due in 3–5 years and $5 million due over 5 years) of unrecognized tax benefits recorded

under FIN No. 48, which we adopted on September 1, 2007.