Walmart 2005 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2005 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

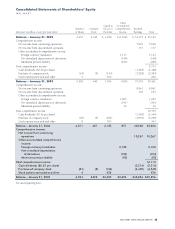

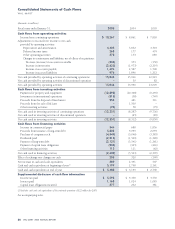

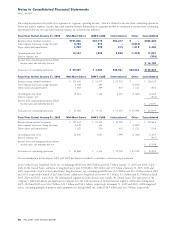

Notes to Consolidated Financial Statements

W A L -M A R T

40 WAL-MART 2005 ANNUAL REPORT

the provisions of SFAS 123(R) upon its release. Prior to the adop-

tion of SFAS 123(R), we used the Black-Scholes-Merton formula to

estimate the value of stock options granted to associates. We con-

tinue to use this acceptable option valuation model following our

adoption of SFAS 123(R). SFAS 123(R) requires that the benefits

of tax deductions in excess of recognized compensation cost be

reported as a financing cash flow, rather than as an operating cash

flow as required under previously effective accounting principles

generally accepted in the United States. The adoption of SFAS

123(R) did not have a material impact on our results of operations,

financial position or cash flows.

2 Commercial Paper and Long-term Debt

Information on short-term borrowings and interest rates is as fol-

lows (dollars in millions):

Fiscal year 2005 2004 2003

Maximum amount outstanding

at any month-end $7,782 $4,957 $4,226

Average daily short-term

borrowings $4,823 $1,498 $1,549

Weighted-average interest rate 1.6% 1.1% 1.7%

At January 31, 2005 and 2004, short-term borrowings consisted

of $3.8 billion and $3.3 billion, respectively, of commercial paper.

At January 31, 2005, the company had committed lines of $4.5 bil-

lion with 53 firms and banks, which were used to support commer-

cial paper, and committed and informal lines of credit with various

banks totaling an additional $159 million.

Long-term debt at January 31, consists of (in millions):

Interest Rate Due by Fiscal Year 2005 2004

4.000 – 6.875% Notes due 2010 $ 4,500 $ 3,500

2.792 – 8.000%, Notes due 2007 3,164 2,130

LIBOR less 0.140%

4.550% – 7.250% Notes due 2014 2,883 2,854

4.150 – 5.875% Notes due 2006 2,597 2,597

LIBOR less 0.0425%

4.125% Notes due 2012 2,000 –

5.750% – 7.550% Notes due 2031 1,941 1,912

5.250% Notes due 2036 1,883 –

4.375% Notes due 2008 1,500 1,500

3.375% Notes due 2009 1,000 1,000

5.006% Notes due 2019(1) 500 500

6.200% Notes due 2011(1) 500 500

6.750% Notes due 2024 250 250

6.550% – 7.500% Notes due 2005 – 1,750

8.500% Notes due 2025 – 250

Other (2) 1,128 1,263

$23,846 $20,006

(1) Includes put option.

(2) Includes adjustments to debt hedged by derivatives.

The company has two separate issuances of $500 million debt

with embedded put options. For the first issuance, beginning June

2001, and each year thereafter, the holders of $500 million of the

debt may require the company to repurchase the debt at face

value, in addition to accrued and unpaid interest. The holders of

the other $500 million issuance may put the debt back to the

company at par plus accrued interest at any time. Both of these

issuances have been classified as a current liability in the

Consolidated Balance Sheets.

Under the company’s most significant borrowing arrangements,

the company is not required to observe financial covenants.

However, under certain lines of credit totaling $4.5 billion which

were undrawn as of January 31, 2005, the company has agreed to

observe certain covenants, the most restrictive of which relates to

minimum net worth levels and amounts of additional secured debt

and long-term leases. The company was not in violation of these

covenants at January 31, 2005.

Long-term debt is unsecured except for $68 million, which is col-

lateralized by property with an aggregate carrying value of approxi-

mately $171 million. Annual maturities of long-term debt during

the next five years and thereafter are (in millions):

Fiscal Year Ended January 31, Annual Maturity

2006 $ 3,759

2007 3,400

2008 1,572

2009 1,037

2010 4,774

Thereafter 9,304

Total $ 23,846

The company has entered into sale/leaseback transactions involv-

ing buildings while retaining title to the underlying land. These

transactions were accounted for as financings and are included in

long-term debt and the annual maturities schedule above. The

resulting obligations are amortized over the lease terms. Future

minimum lease payments during the next five years and thereafter

are (in millions):

Fiscal Year Ended January 31, Minimum Payments

2006 $ 20

2007 18

2008 17

2009 11

2010 11

Thereafter 43

Total $ 120

At January 31, 2005 and 2004, the company had trade letters of

credit outstanding totaling $2.6 billion and $2.0 billion, respectively.

These letters of credit were issued primarily for the purchase of inven-

tory. At January 31, 2005 and 2004, the company had standby letters

of credit outstanding totaling $2.0 billion and $1.4 billion, respectively.