Freddie Mac 2014 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2014 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

|

|

58 Freddie Mac

occurs when the modification of a loan results in a reduction in the loan's interest rate. Due to the large number of

modifications completed in recent years, the portion of our loan loss reserves attributable to TDRs remains high. The reserves

associated with TDRs largely reflect interest rate concessions for the borrower. As of December 31, 2014, approximately 51%

of the loan loss reserves for single-family loans relates to interest rate concessions associated with TDRs. Most of our modified

loans (including TDRs) were current and performing at December 31, 2014. Loans that have been classified as TDRs remain

categorized as such throughout the remaining life of the loan regardless of whether the borrower makes payments which return

the loan to a current payment status. We maintain a loan loss reserve on TDRs until the loans are repaid or complete short sales

or foreclosures. We expect the number of TDRs to remain at elevated levels for the foreseeable future. For information on our

accounting for TDRs, see "NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES — Troubled Debt

Restructurings."

Although the housing market continued to improve in many geographic areas in 2014, we expect that our loan loss

reserves may remain elevated for an extended period because: (a) a significant portion of our reserves is associated with

individually impaired loans (e.g., modified loans) that are less than three months past due; and (b) the resolution of problem

loans takes considerable time, often several years in the case of foreclosure.

Loans that have been individually evaluated for impairment generally have a higher associated loan loss reserve than

loans that have been collectively evaluated for impairment. As of December 31, 2014 and 2013, the recorded investment of

single-family impaired loans with specific reserves recorded was 95.1 billion and 93.7 billion, respectively, and the loan loss

reserves associated with these loans were $17.8 billion and $18.6 billion, respectively.

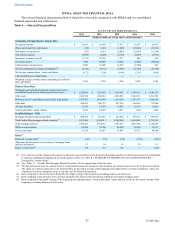

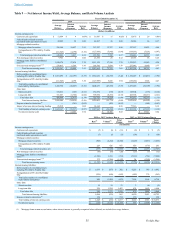

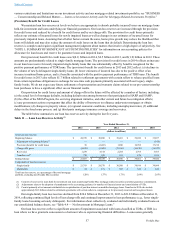

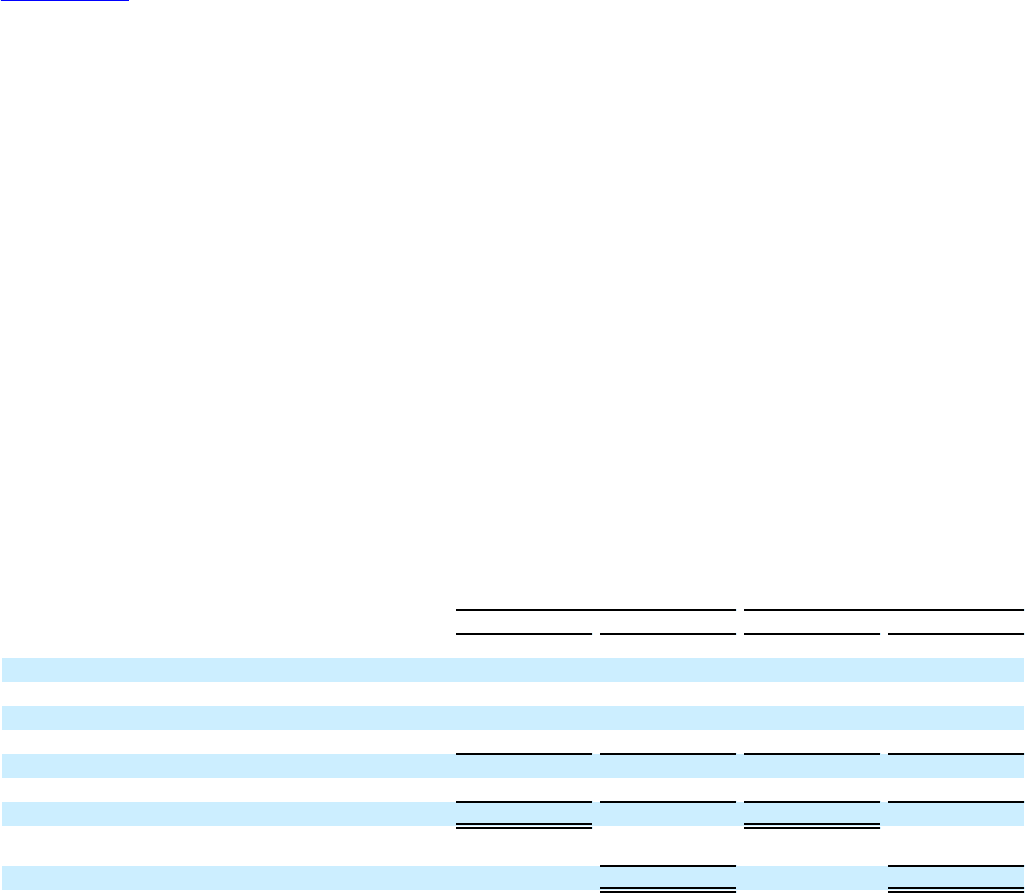

The table below summarizes our net investment for individually impaired single-family mortgage loans on our

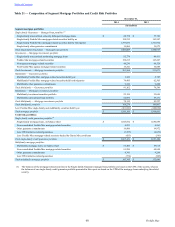

consolidated balance sheets for which we have recorded a specific reserve.

Table 12 — Single-Family Impaired Loans with Specific Reserve Recorded

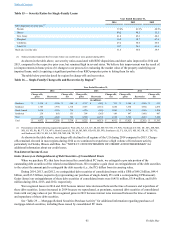

2014 2013

Number of Loans Amount Number of Loans Amount

(dollars in millions)

TDRs, at January 1, 514,497 $ 92,505 449,145 $ 83,484

New additions 84,334 12,581 129,428 20,234

Repayments and reclassifications to held-for-sale (33,104) (6,218) (29,877) (5,074)

Foreclosure transfers and foreclosure alternatives (26,137) (4,467) (34,199) (6,139)

TDRs, at December 31, 539,590 94,401 514,497 92,505

Loans impaired upon purchase 9,949 741 13,790 1,195

Total impaired loans with specific reserve 549,539 95,142 528,287 93,700

Total allowance for loan losses of individually impaired single-

family loans (17,837) (18,554)

Net investment, at December 31, $ 77,305 $ 75,146

We place loans, including TDRs, on non-accrual status when we believe the collectability of interest and principal on a

loan is not reasonably assured, unless the loan is well secured and in the process of collection. When a loan is placed on non-

accrual status, interest income is recognized only upon receipt of cash payments and any interest income accrued but

uncollected is reversed. See “RISK MANAGEMENT — Credit Risk Overview — Single-Family Mortgage Credit Risk

Framework and Profile” for further information on our single-family credit guarantee portfolio, including credit performance,

and seriously delinquent loans. See “NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES” and “NOTE 5:

IMPAIRED LOANS” for further information about our TDRs and non-accrual and other impaired loans.

Table of Contents