Freddie Mac 2014 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2014 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

|

|

83 Freddie Mac

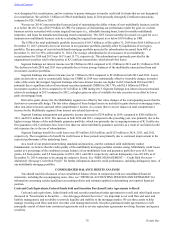

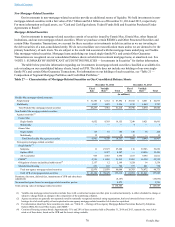

While it is reasonably possible that collateral losses on our available-for-sale securities where we have not recorded an

impairment charge in earnings could exceed our credit enhancement levels, we do not believe that those conditions were likely

at December 31, 2014. As a result, we have concluded that the reduction in fair value of these securities was temporary at

December 31, 2014 and have recorded these unrealized losses in AOCI.

The credit performance of loans underlying our holdings of non-agency mortgage-related securities has declined since

2007 and, although it has stabilized in recent periods, it remains weak. This decline has been particularly severe for subprime,

option ARM, and Alt-A and other loans. Our investments in non-agency mortgage-related securities have at times been

adversely affected by high unemployment, a large inventory of seriously delinquent mortgage loans and unsold homes, tight

credit conditions, and weak consumer confidence. In addition, the loans which serve as collateral for the securities we hold

have significantly greater concentrations in the states that have undergone the greatest economic stress during the housing crisis

that began in 2006, such as California and Florida.

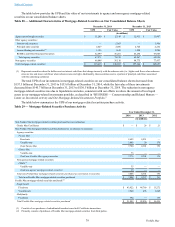

Our assessments concerning other-than-temporary impairment involve the use of models, require significant judgment

and are subject to potentially significant change as conditions evolve. In addition, changes in the performance of the individual

securities and in mortgage market conditions may also affect our impairment assessments. Depending on the structure of the

individual mortgage-related security and our estimate of collateral losses relative to the amount of credit support expected to be

available for the tranches we own, a change in collateral loss estimates can have a disproportionate impact on the loss estimate

for the security. Servicer performance, loan modification programs and backlogs, and various forms of government intervention

in the housing market can significantly affect the performance of these securities, including the timing of loss recognition of the

underlying loans and thus the timing of losses we recognize on our securities. Impacts related to changes in interest rates may

affect our losses due to the structural credit enhancements on our investments in non-agency mortgage-related securities. The

lengthening of the foreclosure timelines that has occurred in recent years can also affect our losses. For example, while

defaulted loans remain in the trusts prior to completion of the foreclosure process, the subordinate classes of securities issued

by the securitization trusts may continue to receive interest payments, rather than absorbing default losses. This may reduce the

amount of funds available for the tranches we own. Given the uncertainty and volatility of the economic environment, it is

difficult to estimate the future performance of mortgage loans and mortgage-related securities with high assurance, and actual

results could differ materially from our expectations. Furthermore, various market participants could arrive at materially

different conclusions regarding estimates of future principal cash shortfalls.

For more information on risks associated with the use of models, see “RISK FACTORS — Operational Risks — We face

risks and uncertainties associated with the models that we use for financial accounting and reporting purposes, to make

business decisions, and to manage risks. Market conditions have raised these risks and uncertainties.”

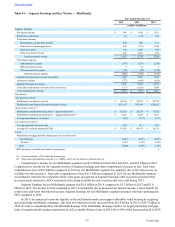

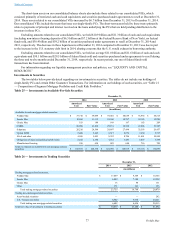

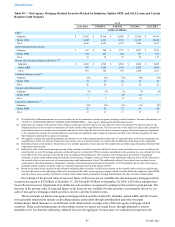

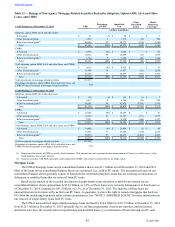

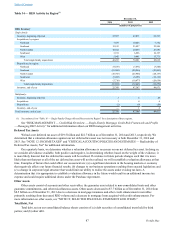

Ratings of Non-Agency Mortgage-Related Securities

The table below shows the ratings of non-agency mortgage-related securities backed by subprime, option ARM, Alt-A

and other loans, and CMBS held at December 31, 2014 based on their ratings as of December 31, 2014, as well as those held at

December 31, 2013 based on their ratings as of December 31, 2013. Ratings presented represent the lower of S&P, Fitch and

Moody's credit ratings, with Fitch and Moody's stated in terms of the S&P equivalent.

Table of Contents