American Airlines 2009 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2009 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

41

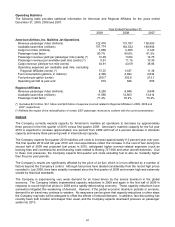

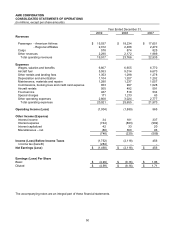

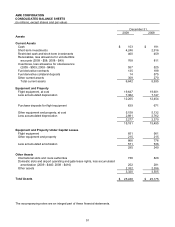

Operating Statistics

The following table provides statistical information for American and Regional Affiliates for the years ended

December 31, 2009, 2008 and 2007.

Year Ended December 31,

2009

2008

2007

American Airlines, Inc. Mainline Jet Operations

Revenue passenger miles (millions)

122,418

131,757

138,453

Available seat miles (millions)

151,774

163,532

169,906

Cargo ton miles (millions)

1,656

2,005

2,122

Passenger load factor

80.7%

80.6%

81.5%

Passenger revenue yield per passenger mile (cents) (^)

12.28

13.84

12.75

Passenger revenue per available seat mile (cents) (^)

9.91

11.15

10.39

Cargo revenue yield per ton mile (cents)

34.91

43.59

38.86

Operating expenses per available seat mile, excluding

Regional Affiliates (cents) (*)

12.22

13.87

11.38

Fuel consumption (gallons, in millions)

2,499

2,694

2,834

Fuel price per gallon (cents)

200.7

302.6

212.1

Operating aircraft at year-end

610

626

655

Regional Affiliates

Revenue passenger miles (millions)

8,255

8,846

9,848

Available seat miles (millions)

11,566

12,603

13,414

Passenger load factor

71.4%

70.2%

73.4%

(*) Excludes $2.5 billion, $3.1 billion and $2.8 billion of expense incurred related to Regional Affiliates in 2009, 2008 and

2007, respectively.

(^) Reflects the impact of the reclassification of certain 2007 passenger revenues to conform with the current presentation.

Outlook

The Company currently expects capacity for American’s mainline jet operations to decrease by approximately

three percent in the first quarter of 2010 versus first quarter 2009. American’s mainline capacity for the full year

2010 is expected to increase approximately one percent from 2009 with half of a percent decrease in domestic

capacity and nearly three percent growth in international capacity.

The Company expects first quarter 2010 mainline unit costs to increase approximately 9.2 percent year over year.

The first quarter 2010 and full year 2010 unit cost expectations reflect the increase in the cost of fuel during the

second half of 2009 and projected fuel prices in 2010, anticipated higher revenue-related expenses (such as

booking fees and commissions) and financing costs related to Boeing 737-800 and other aircraft deliveries. Due

to these cost pressures, the Company expects first quarter unit costs excluding fuel to also be modestly higher

than the prior year periods.

The Company’s results are significantly affected by the price of jet fuel, which is in turn affected by a number of

factors beyond the Company’s control. Although fuel prices have abated considerably from the record high prices

recorded in July 2008, they have steadily increased since the first quarter of 2009 and remain high and extremely

volatile by historical standards.

The Company is experiencing very weak demand for air travel driven by the severe downturn in the global

economy. The Company initially implemented capacity reductions in 2008 and again in the first half of 2009 in

response to record high fuel prices in 2008 and a rapidly deteriorating economy. Those capacity reductions have

somewhat mitigated this weakening of demand. However, if the global economic downturn persists or worsens,

demand for air travel may continue to weaken. No assurance can be given that capacity reductions or other steps

the Company may take will be adequate to offset the effects of reduced demand. In addition, fare discounting has

recently been both broader and deeper than usual, and the Company expects downward pressure on passenger

yields into 2010.