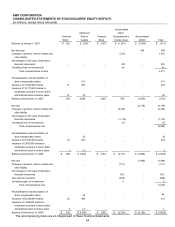

American Airlines 2009 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2009 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

46

ITEM 7(A). QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Market Risk Sensitive Instruments and Positions

The risk inherent in the Company’s market risk sensitive instruments and positions is the potential loss arising

from adverse changes in the price of fuel, foreign currency exchange rates and interest rates as discussed below.

The sensitivity analyses presented do not consider the effects that such adverse changes may have on overall

economic activity, nor do they consider additional actions management may take to mitigate the Company’s

exposure to such changes. Therefore, actual results may differ. The Company does not hold or issue derivative

financial instruments for trading purposes. See Note 7 to the consolidated financial statements for accounting

policies and additional information regarding derivatives.

Aircraft Fuel The Company’s earnings are substantially affected by changes in the price and availability of

aircraft fuel. In order to provide a measure of control over price and supply, the Company trades and ships fuel

and maintains fuel storage facilities to support its flight operations. The Company also manages the price risk of

fuel costs primarily by using jet fuel and heating oil hedging contracts. Market risk is estimated as a hypothetical

10 percent increase in the December 31, 2009 and 2008 cost per gallon of fuel. Based on projected 2010 fuel

usage, such an increase would result in an increase to Aircraft fuel expense of approximately $499 million in 2010,

inclusive of the impact of effective fuel hedge instruments outstanding at December 31, 2009, and assumes the

Company’s fuel hedging program remains effective. Such an increase would have resulted in an increase to

projected Aircraft fuel expense of approximately $399 million in 2009, inclusive of the impact of fuel hedge

instruments outstanding at December 31, 2008. As of January 2010, the Company had cash flow hedges, with

collars and options, covering approximately 24 percent of its estimated 2010 fuel requirements. Comparatively, as

of December 31, 2008, the Company had hedged, with collars and options, approximately 35 percent of its

estimated 2009 fuel requirements. The consumption hedged for 2010 by cash flow hedges is capped at an

average price of approximately $2.48 per gallon of jet fuel, and the Company’s collars have an average floor price

of approximately $1.80 per gallon of jet fuel (both the capped and floor price exclude taxes and transportation

costs). The Company’s collars represent approximately 22 percent of its estimated 2010 fuel requirements. A

deterioration of the Company’s financial position could negatively affect the Company’s ability to hedge fuel in the

future.

Ineffectiveness is inherent in hedging jet fuel with derivative positions based in crude oil or other crude oil related

commodities. The Company assesses, both at the inception of each hedge and on an ongoing basis, whether the

derivatives that are used in its hedging transactions are highly effective in offsetting changes in cash flows of the

hedged items. In doing so, the Company uses a regression model to determine the correlation of the change in

prices of the commodities used to hedge jet fuel (e.g., NYMEX Heating oil) to the change in the price of jet fuel.

The Company also monitors the actual dollar offset of the hedges’ market values as compared to hypothetical jet

fuel hedges. The fuel hedge contracts are generally deemed to be ―highly effective‖ if the R-squared is greater

than 80 percent and the dollar offset correlation is within 80 percent to 125 percent. The Company discontinues

hedge accounting prospectively if it determines that a derivative is no longer expected to be highly effective as a

hedge or if it decides to discontinue the hedging relationship.

Foreign Currency The Company is exposed to the effect of foreign exchange rate fluctuations on the U.S.

dollar value of foreign currency-denominated operating revenues and expenses. The Company’s largest

exposure comes from the British pound, Euro, Canadian dollar, Japanese yen and various Latin American

currencies. The Company does not currently have a foreign currency hedge program related to its foreign

currency-denominated ticket sales. A uniform 10 percent strengthening in the value of the U.S. dollar from

December 31, 2009 and 2008 levels relative to each of the currencies in which the Company has foreign currency

exposure would result in a decrease in operating income of approximately $136 million and $146 million for the

years ending December 31, 2009 and 2008, respectively, due to the Company’s foreign-denominated revenues

exceeding its foreign-denominated expenses. This sensitivity analysis was prepared based upon projected 2010

and 2009 foreign currency-denominated revenues and expenses as of December 31, 2009 and 2008,

respectively.

On January 11, 2010, the Venezuelan Government devalued its currency from 2.15 bolivars per U.S. dollar to

4.30 bolivars per U.S. dollar and the currency was designated as hyperinflationary. As a result, the Company

recognized a loss of $53 million related to the currency remeasurement in January 2010. The Company does not

expect any significant ongoing impact of the currency devaluation on its operations in Venezuela, but there can be

no assurances to that effect.