Kohl's 2009 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2009 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

Table of Contents

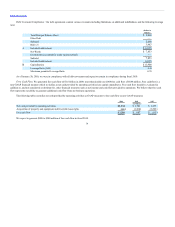

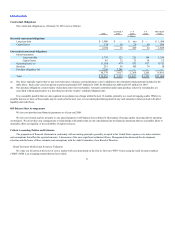

Partially offsetting these expense reductions were higher fixed occupancy and variable store costs due primarily to an increase in the number of stores

and higher accrued incentive expenses as a result of improved performance for 2009 and changes to our non-management compensation structure.

SG&A for 2008 increased $239 million, or 6.5%, over 2007. The net increase in SG&A dollars reflects incremental costs at newly-opened stores,

partially offset by decreases at comparable stores reflecting our commitment to control costs in a difficult economic environment. SG&A increased more than

sales, but less than new store growth of 8.1%.

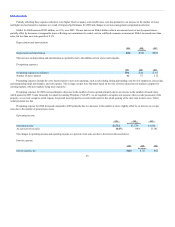

Depreciation and amortization.

Depreciation and amortization $541 $452

The increases in depreciation and amortization are primarily due to the addition of new stores and remodels.

Preopening expenses.

Preopening expenses (in millions) $42 $61

Number of stores opened 75 112

Preopening expenses include the costs incurred prior to new store openings, such as advertising, hiring and training costs for new employees, processing

and transporting initial merchandise, and rent expense. The average cost per store fluctuates based on the mix of stores opened in new markets compared to

existing markets, with new markets being more expensive.

Preopening expenses for 2009 increased despite a decrease in the number of stores opened primarily due to an increase in the number of leased stores

which opened in 2009. Under Generally Accepted Accounting Principles (“GAAP”), we are required to recognize rent expense when we take possession of the

property, so we must recognize rental expense for ground leased properties several months prior to the actual opening of the store and, in most cases, before

rental payments are due.

Preopening expense for 2008 decreased compared to 2007 primarily due to a decrease in the number of stores slightly offset by an increase in cost per

store due to the number of ground lease stores.

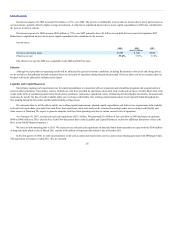

Operating income.

Operating income $1,536 $1,804

As a percent of net sales 9.4% 11.0%

The changes in operating income and operating income as a percent of net sales are due to the factors discussed above.

Interest expense.

Interest expense, net $111 $62

25