LabCorp 2008 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2008 LabCorp annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58

|

|

Notes to Consolidated Financial Statements

(Dollars and shares in millions, except per share data)

Laboratory Corporation of America

54 Laboratory Corporation of America® Holdings 2008

expense. APB 14-1 is effective for financial statements issued for fiscal years beginning after

December 15, 2008, and interim periods within those fiscal years. Retrospective application to

all periods presented is required except for instruments that were not outstanding during any of

the periods that will be presented in the annual financial statements for the period of adoption

but were outstanding during an earlier period. APB 14-1 impacts the Company’s zero-coupon

subordinated notes, and will require that additional interest expense essentially equivalent to

the portion of issuance proceeds retroactively allocated to the instrument’s equity component

be recognized over the period from the zero-coupon subordinated notes’ issuance in 2001 through

September 2004 (the first date holders of these notes had the ability to put them back to the

Company). The Company has evaluated the impact of APB 14-1 and anticipates that its retro-

spective application will have no impact on results of operations for periods following 2004, but

will result in an increase in opening additional paid-in capital and a corresponding decrease in

opening retained earnings, net of deferred tax impacts, on post-2004 consolidated balance sheets.

In October 2008, the FASB issued FASB Staff Position No. FAS 157-3, “Determining the

Fair Value of a Financial Asset When the Market for That Asset Is Not Active” (“FSP 157-3”).

FSP 157-3 clarified the application of SFAS No. 157 in an inactive market. It demonstrated how

the fair value of a financial asset is determined when the market for that financial asset is

inactive. FSP 157-3 was effective upon issuance, including prior periods for which financial

statements had not been issued. The implementation of this standard did not have a material

impact on our consolidated financial position and results of operations.

In December 2008, the FASB issued FASB Staff Position No. FAS 132(R)-1, “Employers’

Disclosures about Postretirement Benefit Plan Assets” (“FSP 132(R)-1”). FSP 132(R)-1

applies to an employer that is subject to the disclosure requirements of SFAS No. 132(R). The

objectives of the disclosures about plan assets in an employers’ defined benefit pension or

other postretirement plan are to provide users of financial statements with an understanding

of: (1) how investment allocation decisions are made, including the factors that are pertinent

to an understanding of investment policies and strategies, (2) the major categories of plan

assets, (3) the inputs and valuation techniques used to measure the fair value of plan assets,

(4) the effect of fair value measurements using significant unobservable inputs (Level 3) on

changes in plan assets for the period, and (5) significant concentrations of risk within plan

assets. An employer should consider those overall objectives in providing detailed disclosures

about plan assets. FSP 132(R)-1 is effective for years ending after December 15, 2009. Early

application is permitted. Upon initial application, the provisions of FSP 132(R)-1 are not required

for earlier periods that are presented for comparative periods. The Company is currently evaluating

the impact the adoption of FSP 132(R)-1 could have on its consolidated financial statements.

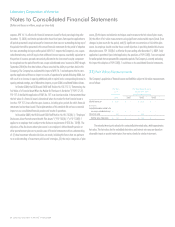

21) Fair Value Measurements

The Company’s population of financial assets and liabilities subject to fair value measurements

are as follows:

Fair Value Fair Value Measurements at

as of December 31, 2008

December 31, Using Fair Value Hierarchy

2008 Level 1 Level 2 Level 3

Minority interest put $ 121.3 $ – $ 121.3 $ –

Derivatives

Embedded derivatives related to the

zero-coupon subordinated notes $ – $ – $ – $ –

Interest rate swap 13.5 – 13.5 –

Total fair value of derivatives $ 13.5 $ – $ 13.5 $ –

The minority interest put is valued at its contractually determined value, which approximates

fair value. The fair values for the embedded derivatives and interest rate swap are based on

observable inputs or quoted market prices from various banks for similar instruments.