Starbucks 2008 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2008 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

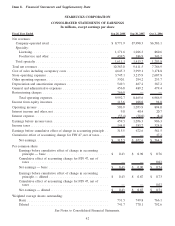

Included in the cash and liquid investment balances are the following:

• A portfolio of unrestricted trading securities, designed to hedge the Company’s liability under its Man-

agement Deferred Compensation Plan (“MDCP”). The value of this portfolio was $49.5 million and

$73.6 million as of September 28, 2008 and September 30, 2007, respectively. The decrease was driven by

the sale of a bond income fund to better align with the Company’s total risk profile and declines in market

values of the underlying equity funds, which were offset by a comparable decline in the MDCP liability.

• Unrestricted cash and liquid securities, held within the Company’s wholly owned captive insurance

company, to fund claim payouts. The value of these unrestricted cash and liquid securities was approx-

imately $35.6 million and $98.1 million as of September 28, 2008 and September 30, 2007, respectively. The

decrease was due primarily to reclassification of auction rate securities held by the wholly owned captive.

As described in more detail in Note 4 to the consolidated financial statements, as of September 28, 2008, the

Company had $74.4 million invested in available-for-sale securities, consisting primarily of auction rate securities.

While the ongoing auction failures will limit the liquidity of these investments for some period of time, the

Company does not believe the auction failures will materially impact its ability to fund its working capital needs,

capital expenditures or other business requirements.

The Company manages the balance of its cash and liquid investments in order to internally fund operating needs and

make scheduled interest and principal payments on its borrowings.

Following the Company’s announcement on July 1, 2008 that it planned to close approximately 600 underperforming

US Company-operated stores and reduce new store growth in fiscal year 2009, Standard & Poor’s placed the BBB+ long-

term rating and A-2 short term ratings for Starbucks on CreditWatch with negative implications. On July 3, 2008,

Moody’s placed the Baa1 senior unsecured rating for Starbucks on review for possible downgrade, however Moody’s

reaffirmed the Company’s Prime-2 short-term rating for commercial paper. Standard and Poor’s and Moody’s

subsequently downgraded the long-term ratings as of September 4, 2008 and November 17, 2008, respectively.

Credit rating agencies currently rate the Company’s borrowings as follows:

Description Standard & Poor’s Moody’s

Short term debt ......................................... A-2 P-2

Senior unsecured long term debt ............................ BBB Baa2

Outlook............................................... Stable Negative

• Standard & Poor’s downgraded the Company’s long-term rating from BBB+ to BBB on September 4, 2008,

and re-affirmed the A-2 short-term rating. At the same time, Standard & Poor’s outlook was changed to

stable.

• Moody’s downgraded the Company’s long-term rating from Baa1 to Baa2 on November 17, 2008, and re-

affirmed the Company’s Prime-2 short term rating for commercial paper. At the same time, Moody’s outlook

was changed to negative.

Factors that may affect credit ratings include changes in the Company’s operating performance, the economic

environment and the Company’s capital structure. In order to maintain its credit ratings, there is an expectation that

the Company will modestly reduce its leverage during fiscal 2009. The Company expects to improve its leverage

ratio below a certain target level primarily through the reduction in short term borrowings. Credit rating downgrades

can adversely impact, among other things, future borrowing costs, access to capital markets, and future operating

lease terms. If either of the Company’s short-term ratings were downgraded, it would likely make the issuance of

commercial paper difficult. In these circumstances the Company could draw upon its credit facility.

In normal market conditions, it is generally more favorable for the Company to issue commercial paper rather than

borrow against the credit facility. However, as described in Item 1A Risk Factors the ongoing global financial crisis

may result in conditions where commercial paper is not available at reasonable rates. In such situations the

Company is more likely to draw on its credit facility. During the fourth quarter of fiscal 2008, the Company

borrowed against the credit facility as liquidity conditions in the commercial paper market deteriorated. As of

September 28, 2008, borrowings outstanding under the credit facility totaled $300 million.

35