Starbucks 2008 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2008 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

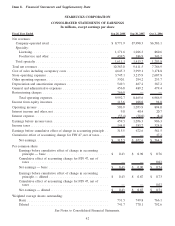

Equity Security Price Risk

The Company has minimal exposure to price fluctuations on equity mutual funds within its trading portfolio. The

trading securities approximate a portion of the Company’s liability under the MDCP. A corresponding liability is

included in “Accrued compensation and related costs” on the consolidated balance sheets. These investments are

recorded at fair value with unrealized gains and losses recognized in “Interest income and other, net” in the

consolidated statements of earnings. The offsetting changes in the MDCP liability are recorded in “General and

administrative expenses.” The Company performed a sensitivity analysis based on a 10% change in the underlying

equity prices of its investments, as of the end of fiscal 2008, and determined that such a change would not have a

significant effect on the fair value of these instruments.

Interest Rate Risk

The Company utilizes short-term and long-term financing and may use interest rate hedges to manage the effect of

interest rate changes on its existing debt as well as the anticipated issuance of new debt. At the end of fiscal years

2008 and 2007, the Company did not have any interest rate hedge agreements outstanding.

The following table summarizes the impact of a change in interest rates on the fair value of the Company’s debt (in

millions):

September 28, 2008

Fair Value

100 Basis Point Increase in

Underlying Rate

100 Basis Point Decrease in

Underlying Rate

Change in Fair Value

Debt ........................ $1,251 (35) 35

The Company’s available-for-sale securities comprise a diversified portfolio consisting mainly of fixed income

instruments. The primary objectives of these investments are to preserve capital and liquidity. Available-for-sale

securities are investment grade and are recorded on the consolidated balance sheets at fair value with unrealized

gains and losses reported as a separate component of “Accumulated other comprehensive income.” The Company

does not hedge the interest rate exposure on its available-for-sale securities. The Company performed a sensitivity

analysis based on a 100 basis point change in the underlying interest rate of its available-for-sale securities as of the

end of fiscal 2008, and determined that such a change would not have a significant effect on the fair value of these

instruments.

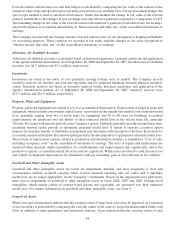

APPLICATION OF CRITICAL ACCOUNTING POLICIES

Critical accounting policies are those that management believes are both most important to the portrayal of the

Company’s financial condition and results, and require management’s most difficult, subjective or complex

judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain.

Judgments and uncertainties affecting the application of those policies may result in materially different amounts

being reported under different conditions or using different assumptions.

Starbucks considers its policies on asset impairment, stock-based compensation, operating leases, self insurance

reserves and income taxes to be the most critical in understanding the judgments that are involved in preparing its

consolidated financial statements.

Asset Impairment

When facts and circumstances indicate that the carrying values of long-lived assets may be impaired, an evaluation

of recoverability is performed by comparing the carrying values of the assets to projected future cash flows, in

addition to other quantitative and qualitative analyses. For goodwill and other intangible assets, impairment tests are

performed annually and more frequently if facts and circumstances indicate goodwill carrying values exceed

estimated reporting unit fair values and if indefinite useful lives are no longer appropriate for the Company’s

trademarks. Upon indication that the carrying values of such assets may not be recoverable, the Company

recognizes an impairment loss as a charge against current operations. Judgments made by the Company related to

39