Starbucks 2008 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2008 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

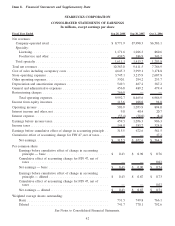

FINANCIAL RISK MANAGEMENT

Market risk is defined as the risk of losses due to changes in commodity prices, foreign currency exchange rates,

equity prices, and interest rates. The Company manages its exposure to various market-based risks according to an

umbrella risk management policy. Under this policy, market-based risks are quantified and evaluated for potential

mitigation strategies, such as entering into hedging transactions. The umbrella risk management policy governs the

hedging instruments the business may use and limits the dollar risk to net earnings. The Company also monitors and

limits the amount of associated counterparty credit risk. Additionally, this policy restricts, among other things, the

amount of market-based risk the Company will tolerate before implementing approved hedging strategies and

prohibits speculative trading activity. In general, hedge instruments do not have maturities in excess of five years.

The sensitivity analyses performed below provide only a limited, point-in-time view of the market risk of the

financial instruments discussed. The actual impact of the respective underlying rates and price changes on the

financial instruments may differ significantly from those shown in the sensitivity analyses.

Commodity Price Risk

The Company purchases commodity inputs, including coffee and dairy products that are used in its operations and

are subject to price fluctuations that impact its financial results. In addition to fixed-priced contracts and price-to-

be-fixed contracts for coffee purchases, the Company may enter into commodity hedges to manage commodity

price risk using financial derivative instruments. The Company performed a sensitivity analysis based on a 10%

change in the underlying commodity prices of its commodity hedges, as of the end of fiscal 2008, and determined

that such a change would not have a significant effect on the fair value of these instruments.

Foreign Currency Exchange Risk

The majority of the Company’s revenue, expense and capital purchasing activities are transacted in US dollars.

However, because a portion of the Company’s operations consists of activities outside of the United States, the

Company has transactions in other currencies, primarily the Canadian dollar, British pound sterling, euro, and

Japanese yen. As a result, Starbucks may engage in transactions involving various derivative instruments to hedge

revenues, inventory purchases, assets, and liabilities denominated in foreign currencies.

As of September 28, 2008, the Company had forward foreign exchange contracts that hedge portions of anticipated

international revenue streams and inventory purchases. In addition, Starbucks had forward foreign exchange

contracts that qualify as accounting hedges of its net investment in Starbucks Japan, as well as the Company’s net

investments in its Canada, UK, and China subsidiaries, to minimize foreign currency exposure.

The Company also had forward foreign exchange contracts that are not designated as hedging instruments for

accounting purposes (free standing derivatives), but which largely offset the financial impact of translating certain

foreign currency denominated payables and receivables. Increases or decreases in the fair value of these hedges are

generally offset by corresponding decreases or increases in the US dollar value of the Company’s foreign currency

denominated payables and receivables (i.e. “hedged items”) that would occur within the hedging period.

The following table summarizes the potential impact to the Company’s future net earnings and other comprehensive

income (“OCI”) from changes in the fair value of these derivative financial instruments due in turn to a change in the

value of the US dollar as compared to the level of foreign exchange rates. The information provided below relates

only to the hedging instruments and does not represent the corresponding changes in the underlying hedged items

(in millions):

September 28, 2008

10% Increase in

Underlying Rate

10% Decrease in

Underlying Rate

10% Increase in

Underlying Rate

10% Decrease in

Underlying Rate

Increase/(Decrease) to Net Earnings Increase/(Decrease) to OCI

Foreign currency hedges............. $68 (56) 15 (19)

38