Walgreens 2004 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2004 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

|

|

27

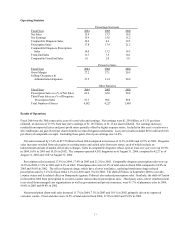

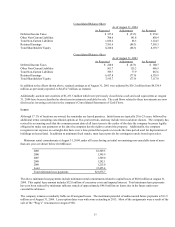

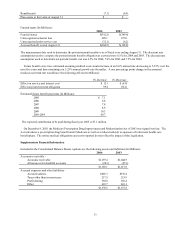

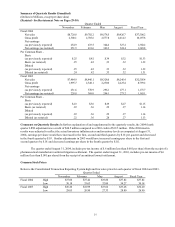

Revenue Recognition

For all sales other than third party pharmacy sales, the company recognizes revenue at the time of the sale. For third party sales,

revenue is recognized at the time the prescription is filled, adjusted by an estimate for those that have not yet been claimed by

customers at the end of the period. Customer returns are immaterial.

Impaired Assets and Liabilities for Store Closings

The company tests long-lived assets for impairment whenever events or circumstances indicate. Store locations that have been

open at least five years are periodically reviewed for impairment indicators. Once identified, the amount of the impairment is

computed by comparing the carrying value of the assets to the fair value, which is based on the discounted estimated future cash

flows. Included in selling, occupancy and administration expense were impairment charges of $9.2 million in 2004, $19.5 million in

2003, and $8.4 million in 2002.

During the fourth quarter of fiscal 2002, the company implemented SFAS No. 146, "Accounting for Costs Associated with Exit or

Disposal Activities." Since implementation, the present value of expected future lease costs (net of estimated sublease rent) is

exp ensed when the location is closed. Prior to this, the liability was recognized at the time management made the decision to

relocate or close the store.

Insurance

The company obtains insurance coverage for catastrophic exposures as well as those risks required by law to be insured. It is the

company’ s policy to retain a significant portion of certain losses related to worker’ s compensation, property losses, business

interruptions relating from such losses and comprehensive general, pharmacist and vehicle

liability. Provisions for these losses are

recorded based upon the company’ s estimates for claims incurred. The provisions are estimated in part by considering historical

claims experience, demographic factors and other actuarial assumptions.

Pre-Opening Expenses

Non-capital expenditures incurred prior to the opening of a new or remodeled store are expensed as incurred.

Advertising Costs

Advertising costs, which are reduced by the portion funded by vendors, are expensed as incurred. Net advertising expenses,

which are included in selling, occupancy and administration expense, were $230.9 million in 2004, $174.0 million in 2003 and $64.5

million in 2002. In fiscal 2003 the company adopted EITF Issue No. 02-16, “Accounting by a Customer (including a Reseller) for

Certain Consideration Received from a Vendor,” which shifted a portion of vendor allowances from advertising expense to cost of

sales. The fiscal 2003 impact resulted in an increase to advertising costs of $75.0 million (.23% of total sales), a reduction to cost of

sales of $56.2 million (.17% of total sales), and a reduction to pre-tax earnings and inventory of $18.8 million.

Stock-Based Compensation Plans

As permitted under SFAS No. 123, the company applies Accounting Principles Board (APB) Opinion No. 25 and related

interpretations in accounting for its plans. Under APB Opinion No. 25, compensation expense is recognized for stock option

grants if the exercise price is below the fair value of the underlying stock at the measurement date.

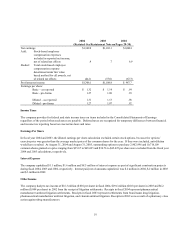

The company complies with the disclosure provisions of SFAS No. 123, which require presentation of pro forma information

applying the fair value based method of accounting. Had compensation costs been determined consistent with the fair value

based method of SFAS No. 123 for options granted in fiscal 2004, 2003 and 2002, pro forma net earnings and net earnings per

common share would have been as follows (In Millions, except per share data):