Walgreens 2009 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2009 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

|

|

2009 Walgreens Annual Report Page 29

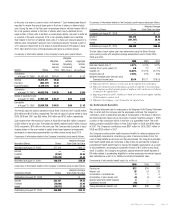

comprehensive general, pharmacist and vehicle liability. Liabilities for these losses are

recorded based upon the Company’s estimates for claims incurred and are not dis-

counted. The provisions are estimated in part by considering historical claims experi-

ence, demographic factors and other actuarial assumptions.

Pre-Opening Expenses

Non-capital expenditures incurred prior to the opening of a new or remodeled store

are expensed as incurred.

Advertising Costs

Advertising costs, which are reduced by the portion funded by vendors, are expensed

as incurred. Net advertising expenses, which are included in selling, general and

administrative expenses, were $334 million in 2009, $341 million in 2008 and $356

million in 2007. Included in net advertising expenses were vendor advertising

allowances of $174 million in 2009, $180 million in 2008 and $170 million in 2007.

Stock-Based Compensation Plans

In accordance with SFAS No. 123(R), Share-Based Payment, the Company recognizes

compensation expense on a straight-line basis over the employee’s vesting period or

to the employee’s retirement eligible date, if earlier.

Total stock-based compensation expense for fiscal 2009, 2008 and 2007 was

$84 million, $68 million and $74 million, respectively. The recognized tax benefit was

$29 million, $23 million and $26 million for fiscal 2009, 2008 and 2007, respectively.

As of August 31, 2009, there was $104 million of total unrecognized compensation

cost related to non-vested awards. This cost is expected to be recognized over a

weighted average of two years.

Income Taxes

We account for income taxes according to the asset and liability method of accounting

for income taxes. Under this method, deferred tax assets and liabilities are recognized

based upon the estimated future tax consequences attributable to differences between

the financial statement carrying amounts of existing assets and liabilities and their

respective tax bases. Deferred tax assets and liabilities are measured pursuant to tax

laws using rates we expect to apply to taxable income in the years in which we expect

those temporary differences to be recovered or settled. The effect on deferred tax

assets and liabilities of a change in tax rate is recognized in income in the period that

includes the enactment date. Valuation allowances are established when necessary to

reduce deferred tax assets to the amounts more likelythan not to be realized.

In determining our provision for income taxes, we use an annual effective income tax

rate based on full-year income, permanent differences between book and tax income,

and statutory income tax rates. The effective income tax rate also reflects our assess-

ment of the ultimate outcome of tax audits. Discrete events such as audit settlements

or changes in tax laws are recognized in the period in which theyoccur.

We are subject to routine income tax audits that occur periodically in the normal

course of business. U.S. federal, state and local and foreign tax authorities raise

questions regarding our tax filing positions, including the timing and amount of

deductions and the allocation of income among various tax jurisdictions. In evaluating

the tax benefits associated with our various tax filing positions, we record a tax benefit

for uncertain tax positions using the highest cumulative tax benefit that is more likely

than not to be realized. Adjustments are made to our liability for unrecognized tax

benefits in the period in which we determine the issue is effectively settled with

the tax authorities, the statute of limitations expires for the return containing the tax

position or when more information becomes available. Our liability for unrecognized

tax benefits, including accrued penalties and interest, is included in other long-term

liabilities on our consolidated balance sheets and in income tax expense in our

consolidated statements of earnings.

We adopted the provisions of FASB Interpretation No. (FIN) 48, Accounting for

Uncertainty in Income Taxes – an Interpretation of FASB Statement No. 109,

effective September 1, 2007. FIN 48 provides guidance regarding the recognition,

measurement, presentation and disclosure in the financial statements of tax positions

taken or expected to be taken on a tax return, including the decision whether to file

or not to file in a particular jurisdiction.

Depreciation expense for property and equipment was $787 million in fiscal 2009,

$697 million in fiscal 2008 and $585 million in fiscal 2007.

The Company capitalizes application stage development costs for significant

internally developed software projects, including “Capacity Management Logistics

Enhancements,” upgrades to merchandise ordering systems, “Store POS,” a store

point of sale system, “POWER,” a workload balancing system, and “Ad Planning,”

an advertising system. These costs are amortized over a five-year period.

Amortization was $40 million in 2009, $36 million in 2008 and $29 million in

2007. Unamortized costs as of August 31, 2009 and 2008, were $202 million

and $173 million, respectively.

Goodwill and Other Intangible Assets

Goodwill represents the excess of the purchase price over the fair value of assets

acquired and liabilities assumed. The Company accounts for goodwill and intangibles

under SFAS No. 142, Goodwill and Other Intangible Assets, which does not permit

amortization, but requires the Company to test goodwill and other indefinite-lived

assets for impairment annually or whenever events or circumstances indicate

impairment may exist.

Revenue Recognition

The Company recognizes revenue at the time the customer takes possession of

the merchandise. Customer returns are immaterial. Sales taxes are not included

in revenue.

The services the Companyprovides to our pharmacy benefit management (PBM)

clients include: plan set-up, claims adjudication with network pharmacies, formulary

management, and reimbursement services. Through its PBM the Company acts as

an agent in administering pharmacy reimbursement contracts and does not assume

credit risk. Therefore, revenue is recognized as only the differential between the

amount receivable from the client and the amount owed to the network pharmacy.

We act as an agent to our clients with respect to administrative fees for claims

adjudication. Those service fees are recognized as revenue.

Gift Cards

The Companysells Walgreens gift cards to our customers in our retail stores and

through our website. Wedo not charge administrative fees on unused gift cards and

our gift cards do not have an expiration date. We recognize income from gift cards

when (1) the gift card is redeemed by the customer; or (2) the likelihood of the gift

card being redeemed bythe customer is remote (“gift card breakage”) and we

determine thatwe do not have a legal obligation to remit the value of unredeemed

gift cards to the relevant jurisdictions. We determine our gift card breakage rate

based upon historical redemption patterns. Gift card breakage income, which is

included in selling, general and administrative expenses, was not significant in

fiscal 2009, 2008 or 2007.

Impaired Assets and Liabilities for Store Closings

The Company tests long-lived assets for impairment whenever events or circum-

stances indicate that a certain asset may be impaired. Store locations that have

been open atleast five years are reviewed for impairment indicators at least annually.

Once identified, the amount of the impairment is computed by comparing the

carrying value of the assets to the fair value, which is based on the discounted

estimated future cash flows. Impairment charges included in selling, general and

administrative expenses were $10 million in 2009, $12 million in 2008 and

$10 million in 2007. The reserve for impaired assets was $47 million, $49 million

and $44 million in fiscal 2009, 2008 and 2007, respectively.

The Company also provides for future costs related to closed locations. The liability

is based on the present value of future rent obligations and other related costs

(net of estimated sublease rent) to the first lease option date. The reserve for store

closings was $99 million, $69 million and $67 million in fiscal 2009, 2008 and

2007, respectively.

Insurance

The Company obtains insurance coverage for catastrophic exposures as well as

those risks required by law to be insured. It is the Company’spolicy to retain a

significant portion of certain losses related to workers’ compensation, property,