Walgreens 2009 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2009 Walgreens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42

|

|

2009 Walgreens Annual Report Page 33

to 101% of the principal amount of the notes plus accrued and unpaid interest to the

date of purchase. The notes are unsecured senior debt obligations and rank equal-

ly with all other unsecured senior indebtedness of the Company. The notes are not

convertible or exchangeable. Total issuance costs relating to this offering were

$8 million, which included $7 million in underwriting fees. The fair value of the notes

as of August 31, 2009, was $1,081 million. Fair value was determined based upon

discounted future cash flows for these notes.

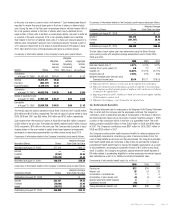

9. Financial Instruments

We use a derivative instrument to manage our interest rate exposure associated

with some of our fixed-rate borrowings. We do not use derivative instruments for

trading or speculative purposes. All derivative instruments are recognized in the

consolidated balance sheets at fair value. We designate interest rate swaps as fair

value hedges of fixed-rate borrowings. For derivatives designated as fair value hedges,

the change in the fair value of both the derivative instrument and the hedged item are

recognized in earnings in the current period. At the inception of a hedge transaction,

we formally document the hedge relationship and the risk management objective for

undertaking the hedge. In addition, we assess both at inception of the hedge and

on an ongoing basis, whether the derivative in the hedging transaction has been

highly effective in offsetting changes in fair value of the hedged item and whether

the derivative is expected to continue to be highly effective. The impact of any

ineffectiveness is recognized currentlyin earnings.

Counterparties to derivative financial instruments expose us to credit-related losses

in the event of nonperformance, but we currently do not expect any counterparties

to fail to meet their obligations given their high credit ratings.

Fair Value Hedges

For derivative instruments that are designated and qualify as fair value hedges, the

gain or loss on the derivative, as well as the offsetting gain or loss on the hedged

item attributable to the hedged risk, are recognized in current earnings.

The notional amounts of derivative instruments outstanding as of August 31, 2009,

were as follows (In millions):

Notional Amount

Derivatives designated as hedges:

Interest rate swaps $1,300

Total derivatives $1,300

The changes in fair value of the bond as a result of the derivative instrument is

included in our long-term debt note (see Note 8) and amortized through maturity.

As of August 31, 2009, we had net unamortized fair value changes of $2 million.

The fair value and balance sheet presentation of derivative instruments as of

August 31, 2009, were as follows (In millions):

Location in

Consolidated Balance Sheet Fair Value

Liability derivatives designated as hedges:

Interest rate swaps Accrued expenses

and other liabilities $2

Total liability derivatives $ 2

Gains and losses on derivative instruments are recorded in interest expense on

our consolidated statement of earnings. The amount recorded for the year ended

August 31, 2009, was immaterial.

10. Fair Value Measurements

SFAS No. 157, Fair Value Measurements, defines fair value as the price that would be

received for an asset or paid to transfer a liability in an orderly transaction between

market participants on the measurement date. SFAS No. 157 establishes a fair value

hierarchy that prioritizes observable and unobservable inputs used to measure fair

value into three broad levels:

Level 1 – Quoted prices in active markets that are accessible at the measurement

date for identical assets and liabilities. The fair value hierarchy gives the

highest priority to Level 1 inputs.

Level 2 – Observable inputs other than quoted prices in active markets.

Level 3 – Unobservable inputs for which there is little or no market data available.

The fair value hierarchy gives the lowest priority to Level 3 inputs.

The fair value of financial assets and liabilities measured at fair value on a recurring

basis was as follows (In millions):

August 31, 2009 Level 1 Level 2 Level 3

Liabilities:

Interest rate swaps $2— $2—

Interest rate swaps are valued using future LIBOR rates.

11. Commitments and Contingencies

The Companyis involved in legal proceedings, and is subject to investigations,

inspections, audits, inquiries and similar actions by governmental authorities, inciden-

tal to the normal course of the Company’sbusiness.

In October 2006, a$31 million judgment was entered against the Companyin Illinois

state court. In March 2009, the Illinois Appellate Court reversed the punitive portion of

the judgment in the amount of $25 million and the Companysettled the balance of

the claim. Other parties of interest in the matter appealed the reversal of the punitive

damages to the Supreme Court of Illinois. The Supreme Court rejected the appeal on

September 30, 2009.

On April 16, 2008, the Plumbers and Steamfitters Local No. 7 Pension Fund filed a

putative class action suit against the Company and its former and current Chief

Executive Officers in the United States District Court for the Northern District of

Illinois. The suit was filed on behalf of purchasers of Companycommon stock during

the period between June 25, 2007, and November 29, 2007. The complaint, which

was amended on October 16, 2008, charged the Company and its former and cur-

rent Chief Executive Officers with violations of Section 10(b) of the Securities

Exchange Act of 1934, claiming that the Company misled investors by failing to dis-

close declining rates of growth in generic drug sales and a contract dispute with a

pharmacy benefits manager that allegedlyhad a negative impact on earnings. The

United States District Court dismissed the suit on September 24, 2009.

On August 31, 2009, a Walgreen Co. shareholder named Dan Himmel filed a lawsuit,

purportedlyon the Company’sbehalf, against several current and former officers and

directors (each, an “Individual Defendant”). The case is captioned Himmel v. Wasson,

et. al. and was filed in the Circuit Court of Lake County,Illinois. The allegations in the

lawsuit are similar to the securities fraud lawsuit described above. Himmel alleges

that Walgreens management: (i) knew, or was reckless in not knowing, that selling,

general and administrative expenses in the fourth quarter of 2007 were too high, in

light of decreased profits from generic drug sales; (ii) knew,or was reckless in not

knowing, that the Company would not realize gross profits near what many Wall

Street analysts were predicting; and (iii) the directors and officers had a duty both to

prevent the drop in gross profits and to disclose the expected drop to the public and

failed to do either. In connection with this lawsuit, Walgreens is advancing each