Unum 2007 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2007 Unum annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

38 Unum 2007 Annual Report

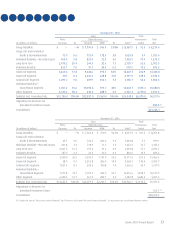

As of December 31, 2007, the key assumptions used to estimate the fair value of private placement fixed maturity securities included

the following:

•Riskfreeinterestratesof3.44percentforve-yearmaturitiesto4.45percentfor30-yearmaturitieswerederivedfromthecurrent

yield curve for U.S. Treasury Bonds with similar maturities.

•CurrentBaacorporatebondspreadsrangingfrom1.81percentto2.15percentplusanadditional20basispointswereaddedtothe

risk free rate to reflect the lack of liquidity.

•Anadditionalvebasispointswereaddedtotheriskfreeratesforforeigninvestments.

•Additionalbasispointswereaddedasdeemedappropriateforcertainindustriesandforindividualsecuritiesincertainindustries

that are considered to be of greater risk.

Increasing the 20 basis points added to the risk free rate for lack of liquidity by 1.5 basis points, increasing the five basis points added

to the risk free rates for foreign investments by one basis point, and increasing the additional basis points added to each industry considered

to be of greater risk by one basis point would have decreased the December 31, 2007 net unrealized gain in the fixed maturity securities

portfolio by approximately $1.7 million. Historically, our realized gains or losses on dispositions of private placement fixed maturity securities

have not varied significantly from amounts estimated under the valuation methodology described above.

Changes in the fair value of fixed maturity securities, other than declines that are determined to be other than temporary, are reported

as a component of other comprehensive income in stockholders’ equity. If we subsequently determine that any of these securities are

other than temporarily impaired, the impairment loss is reported as a realized investment loss in our consolidated statements of income.

The recognition of the impairment loss does not affect total stockholders’ equity to the extent that the decline in value had been previously

reflected in other comprehensive income.

There are a number of significant risks inherent in the process of monitoring our fixed maturity securities for impairments and

determining when and if an impairment is other than temporary. These risks and uncertainties include the following possibilities:

•Theassessmentofaborrower’sabilitytomeetitscontractualobligationswillchange.

•Theeconomicoutlook,eitherdomesticorforeign,maybelessfavorableormayhaveamoresignicantimpactontheborrower

than anticipated, and as such, the security may not recover in value.

•Newinformationmaybecomeavailableconcerningthesecurity,suchasdisclosureofaccountingirregularities,fraud,orcorporate

governance issues.

•Signicantchangesincreditspreadsmayoccurintherelatedindustry.

•Signicantincreasesininterestratesmayoccurandmaynotreturntolevelssimilartowhensecuritieswereinitiallypurchased.

•Adverseratingagencyactionsmayoccur.

Pension and Postretirement Benefit Plans

We sponsor several defined benefit pension and other postretirement benefit (OPEB) plans for our employees, including non-qualified

pension plans. The U.S. pension plans comprise the majority of our total benefit obligation and pension expense. Our U.K. operation

maintains a separate defined benefit plan for eligible employees. The U.K. defined benefit pension plan was closed to new entrants on

December 31, 2002.

We follow Statements of Financial Accounting Standards No. 87 (SFAS 87), Employers’ Accounting for Pensions, No. 106 (SFAS 106),

Employers’ Accounting for Postretirement Benefits Other Than Pensions, No. 132 (SFAS 132), Employers’ Disclosures about Pensions and

Other Postretirement Benefits, and No. 158 (SFAS 158), Employers’ Accounting for Defined Benefit Pension and Other Postretirement

Plans, an amendment of FASB Statements No. 87, 88, 106, and 132(R) in our financial reporting and accounting for our pension and

postretirement benefit plans. See Note 10 of the “Notes to Consolidated Financial Statements” for further discussion.

Our net periodic benefit costs and the value of our benefit obligations for these plans are determined based on a set of economic

and demographic assumptions that represent our best estimate of future expected experience. Major assumptions used in accounting

for these plans include the expected discount (interest) rate and the long-term rate of return on plan assets. We also use, as applicable,

expected increases in compensation levels and a weighted-average annual rate of increase in the per capita cost of covered benefits,

which reflects a health care cost trend rate.