Unum 2007 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2007 Unum annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

66 Unum 2007 Annual Report

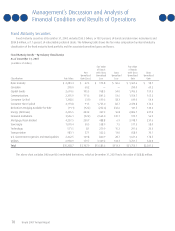

Investments

Overview

Investment activities are an integral part of our business, and profitability is significantly affected by investment results. We segment our

invested assets into portfolios that support our various product lines. Generally, our investment strategy for our portfolios is to match the

effective asset cash flows and durations with related expected liability cash flows and durations to consistently meet the liability funding

requirements of our businesses. We try to maximize investment income and assume credit risk in a prudent and selective manner, subject to

constraints of quality, liquidity, diversification, and regulatory considerations. Our overall investment philosophy is to invest in a portfolio

of high quality assets that provide investment returns consistent with those assumed in the pricing of our insurance products. Assets are

invested predominately in fixed maturity securities, and the portfolio is matched with liabilities so as to eliminate as much as possible our

exposure to changes in the overall level of interest rates. Changes in interest rates may affect the amount and timing of cash flows.

We actively manage our asset and liability cash flow match, as well as our asset and liability duration match to minimize interest rate

risk. We may redistribute investments within our different lines of business, when necessary, to adjust the cash flow and/or duration of

the asset portfolios to better match the cash flow and duration of the liability portfolios. Asset and liability portfolio modeling is updated

on a quarterly basis and is used as part of the overall interest rate risk management strategy. Cash flows from the inforce asset and liability

portfolios are projected at current interest rate levels and also at levels reflecting an increase and a decrease in interest rates to obtain a

range of projected cash flows under the different interest rate scenarios. These results enable us to assess the impact of projected changes

in cash flows and duration resulting from potential changes in interest rates. Testing the asset and liability portfolios under various interest

rate scenarios enables us to choose the most appropriate investment strategy as well as to minimize the risk of disadvantageous outcomes.

This analysis is a precursor to our activities in derivative financial instruments, which are used to hedge interest rate risk and to manage

duration match. At December 31, 2007, the weighted average duration of our policyholder liability portfolio was approximately 8.03 years,

and the weighted average duration of our investment portfolio supporting those policyholder liabilities was approximately 7.26 years.

We believe that our investment portfolio is positioned to lessen the potential impact of an economic slowdown on our financial position

or operating results. Our portfolio is well diversified by type of investment and industry sector. Over the past few years, we have actively

reduced our exposure to below-investment-grade fixed maturity securities, although additional downgrades may occur during an economic

slowdown. Recent market concerns have been centered on several specific types of investment securities. We have no exposure to

subprime mortgages or collateralized debt obligations in our asset-backed or mortgage-backed securities portfolios, our exposure to

“Alt-A” loans within our mortgage-backed securities portfolio is less than $6.0 million, and we hold less than $35.0 million of collateralized

debt obligations within our public bond portfolio. We have approximately $150.0 million of exposure to investments for which the payment

of interest and principal is guaranteed under a financial guaranty insurance policy. The weighted average rating of the underlying securities,

absent the guaranty insurance policy, is A1.

Below is a summary of our formal investment policy, including the overall quality and diversification objectives.

•Themajorityofinvestmentsareinhighqualitypubliclytradedsecuritiestoensurethedesiredliquidityandpreservethecapital

value of our portfolios.

•Thelong-termnatureofourinsuranceliabilitiesalsoallowsustoinvestinlessliquidinvestmentstoobtainsuperiorreturns.

A maximum of 10 percent of the total investment portfolio may be invested in below-investment-grade securities, 2 percent in

equity type instruments, up to 35 percent in private placements, and 5 percent in commercial mortgage loans. The remaining

assets can be held in publicly traded investment-grade corporate securities, mortgage-backed securities, bank loans, asset-backed

securities, government and government agencies, and municipal securities.

•Weintendtomanagetheriskoflossesduetochangesininterestratesbymatchingassetdurationwithliabilities,intheaggregate,

to within a range of +/- ten percent of the liability duration.

•TheweightedaveragecreditqualityratingoftheportfolioshouldbeBBBorhigher.