Unum 2007 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2007 Unum annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

48 Unum 2007 Annual Report

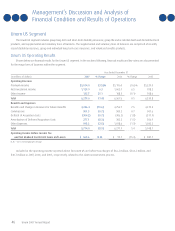

Year Ended December 31, 2006 Compared with Year Ended December 31, 2005

Sales for Unum US increased slightly in 2006 compared to 2005, with a sales mix of approximately 52 percent core market and 48 percent

large case in our group products.

Group disability sales, on a fully insured basis, increased in 2006 compared to 2005, with an increase in the large case market driven

by additional new sales to existing group policyholders. Group disability case coverages in the core market grew relative to 2005, but

because of a lower case size, core market sales, when measured in dollars of annualized premium income, declined relative to 2005.

On a by market segment basis, core market segment sales for group life increased in 2006 relative to 2005, while sales in the large case

market segment decreased in 2006 compared to 2005.

Approximately 90 percent of total 2006 sales for our individual disability line of business occurred in the multi-life market. Long-term

care sales were generally in line with our strategy for this product line, with growth in the group product and a decline in sales for

individual long-term care. Voluntary benefits sales increased in 2006 in comparison to 2005 as we continued to focus on the voluntary

product lines for future growth.

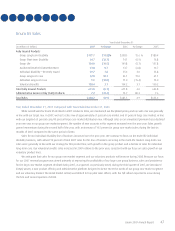

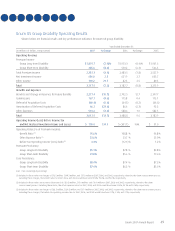

Unum US Persistency and Renewal of Existing Business

A continuing part of our strategy for Unum US group business involves executing our renewal programs and managing persistency in our

existing blocks of business. Our renewal programs have generally been successful in retaining business that is relatively more profitable

than business that terminated. While we believe the additional premium and related profits associated with renewal activity will continue

to emerge, we intend to balance the renewal program with the need to maximize persistency and retain broker relationships. Persistency,

measured in both premium dollars and in number of cases, for the large case group market segment declined during 2007 relative to the

prior year because of our 2007 strategy for this market. Premium persistency was also lower for our core group market segment, but case

persistency for this market segment improved over the level of 2006. During 2006, persistency for each of our product lines was generally

higher than or consistent with 2005.

We adopted the provisions of SOP 05-1 effective January 1, 2007, and recorded a cumulative effect adjustment which decreased our

2007 opening balance of Unum US DAC $589.8 million. SOP 05-1 provides guidance on accounting for DAC on internal replacements and

effectively shortens the amortization period for DAC for many of our group products. Despite the shorter amortization period, we do not

believe that the adoption of SOP 05-1 will have a material effect on amortization expense for Unum US as a result of the decrease in DAC

from the cumulative effect adjustment. We will continue to monitor the persistency of the existing business and reflect changes relative

to our amortization assumptions, as appropriate, in the current period’s amortization of DAC.

In January 2006, we began a process of filing a request with various state insurance departments for rate adjustments on one older

series of individual long-term care policies. The rate adjustment brings the rates for this policy series closer to today’s market, better

reflecting current interest rates, higher expected future claims, persistency, experience, and other factors related to pricing individual

long-term care coverage. In states for which a rate increase is submitted and approved, customers are also given options for coverage

changes or other approaches that might fit their current financial and insurance needs. Higher premium income associated with the rate

increases has begun to emerge and is expected to continue to do so during 2008.