Unum 2007 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2007 Unum annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

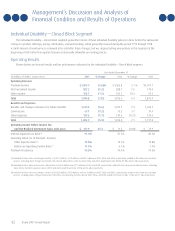

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

60 Unum 2007 Annual Report

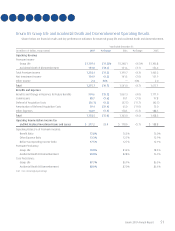

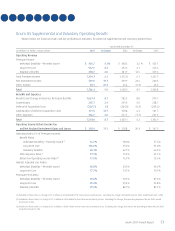

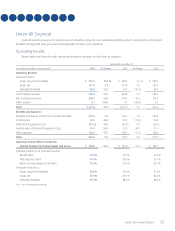

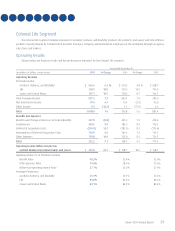

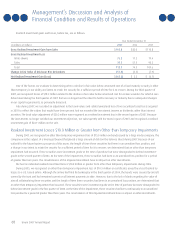

Year Ended December 31, 2007 Compared with Year Ended December 31, 2006

Growth in premium income was attributable primarily to current and prior period sales growth and stable persistency. Net investment

income increased in 2007 in comparison to the prior year due primarily to growth in the level of assets supporting these lines of business.

The benefit ratio for this segment decreased in 2007 in comparison to the prior year due primarily to favorable risk experience in the

accident, sickness, and disability line of business as well as the life line of business. The improvement in the accident, sickness, and disability

line of business resulted from the continued favorable experience related to several new products introduced in 2004. In addition, individual

short-term disability claim incidence and average claim duration decreased in 2007 compared to the prior year, while the average claim

payment was higher in 2007 relative to the prior year. For accident products, the claim incidence rate decreased in 2007 compared to

the prior year, while the average claim payment remained constant in 2007 relative to the prior year. The life line of business reported

a decrease in the rate of incurred claims for 2007, although the aggregate claim expense increased due to the larger block of business.

The cancer and critical illness product line also reported a slightly lower benefit ratio in 2007 relative to the prior year.

Although we continue to focus on expense management, the other expense ratio for 2007 increased in comparison to the prior year

due primarily to our investment in brand and product promotion and the development of additional product offerings. Also, during 2006

we reported a one-time adjustment to commissions and operating expenses that increased reported commissions and reduced other

expenses for that year.

Year Ended December 31, 2006 Compared with Year Ended December 31, 2005

Growth in premium income was attributable primarily to current and prior period sales growth and stable persistency, partially offset

by the lapsing of policies during the first quarter of 2006 for policyholders in hurricane-impacted areas. Net investment income decreased

in 2006 in comparison to 2005 due primarily to the receipt of interest during 2005 on a bond previously in default.

The benefit ratio for this segment decreased in 2006 in comparison to 2005 due primarily to favorable risk experience in the accident,

sickness, and disability line of business. The improvement resulted from underwriting actions taken in 2004 and 2005 as well as the

introduction of several new products in 2004. Sales of these new products increased significantly during 2006. Also favorably impacting

year-over-year comparisons was the first quarter of 2006 release of reserves related to the lapsed policies in the hurricane-impacted

areas and a $3.5 million reserve charge in 2005 related to cancer litigation. In addition, individual short-term disability claim incidence and

average claim duration decreased in 2006 compared to 2005, while the average indemnity on claims was higher in 2006 relative to 2005.

For accident, the claim incidence rate decreased in 2006 relative to 2005, but the average claim payment increased over that reported for

2005. These positive trends were slightly offset by an increase in the claim incidence rate as well as the average claim payment during

2006 for our hospital income product. For cancer, the incidence increased in 2006 relative to 2005, but the incurred loss ratio decreased

due to the introduction of a new cancer product. The life line of business reported a slight increase in the number of paid claims in 2006

relative to 2005 and an increase in the average claim payment.

The other expense ratio for 2006 decreased in comparison to 2005 due primarily to our expense management focus and the

increase in premium income as well as the commission and expense adjustment noted above.