American Express 2001 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2001 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

As is the case with consumer spending, companies tend to continue purchasing

everyday goods and services (such as office and industrial supplies, computer

equipment and software) during tough economic times, while tightening their

belts on discretionary business travel and entertainment expenses.

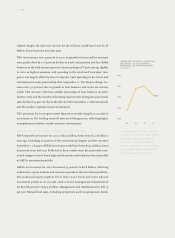

WE HAVE DIVERSIFIED OUR PRODUCT PORTFOLIO AND GROWN OUR

CARD LENDING BUSINESS. Since late 1994, when we set our sights on aggres-

sively expanding our credit card business, our lending balance growth has been

among the top tier of issuers. Today, about 19 percent of our U.S. card billings

come from our lending products, as compared with just 4 percent in 1995. This

change in product mix has shifted our overall card revenue base and helped to

make it less volatile. Revenues from our charge card products are derived from

current spending and are more sensitive to short-term economic swings.

Lending products, on the other hand, produce revenues as customers build up

loan balances and pay them down over time. When credit exposure is managed

prudently, the interest revenue from these products tends to be a less volatile

source of earnings.

At year-end 2001, our worldwide lending balances on a managed basis were

more than $36 billion, up 14 percent from 2000. With $32 billion of receivables

in the United States, our growth rate continued to exceed that of most of our

competitors.

Much of this growth has been due to the breadth of our lending products – such

as our popular Blue from American ExpressSM – and to the value we provide our

cardmembers. We have also increased the number of charge cardmembers who

are taking advantage of our “lending on charge” options such as Sign & Travel®,

when they occasionally choose to revolve.

WE HAVE ACCELERATED OUR REENGINEERING INITIATIVES THROUGH-

OUT THE COMPANY. The reengineering actions we took during 2001 enabled

us to deliver more than $1 billion in gross realized benefits during the year.

The benefits generated by these initiatives serve not only to support earnings

but also to establish the foundation for sustainable, long-term growth. Thus,

while a portion of the savings from reengineering has gone into improving our

axp_11

U.S. BILLINGS ON

REVOLVING CREDIT CARDS

19%

4%

About 19 percent of total U.S.

spending on American Express

Cards last year was on one of

the company’s revolving credit

card products. Attractive terms

and cobrand relationships have

helped to raise this amount from

only 4 percent in 1995.

in 2001

in 1995