American Express 2001 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2001 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

axp_62

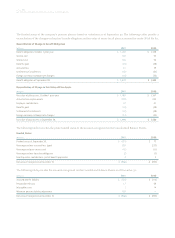

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 10 ❚DERIVATIVES AND HEDGING ACTIVITIES

As prescribed by SFAS No. 133, derivative instruments that are designated and qualify as hedging instruments are further classi-

fied as either a cash flow hedge, a fair value hedge or a hedge of a net investment in a foreign operation, based upon the exposure

being hedged.

For derivative instruments that are designated and qualify as a cash flow hedge, the portion of the gain or loss on the derivative

instrument effective at offsetting changes in the hedged item is reported as a component of other comprehensive income (loss)

and reclassified into earnings when the hedged transaction affects earnings. Any ineffective portion of the gain or loss on the deriv-

ative instrument is recognized currently in earnings. For derivative instruments that are designated and qualify as a fair value

hedge, the gain or loss on the derivative instrument as well as the offsetting loss or gain on the hedged item attributable to the

hedged risk is recognized in current earnings during the period of the change in fair values. For derivative instruments that are

designated and qualify as a hedge of a net investment in a foreign operation, the effective portion of the gain or loss on the deriv-

ative is reported in other comprehensive income (loss) as part of the cumulative translation adjustment. For derivative instruments

not designated as hedging instruments, the gain or loss is recognized currently in earnings.

CASH FLOW HEDGES

The company uses interest rate products, primarily swaps, to manage funding costs related to TRS’ Charge Card business, as well

as AEFA’s investment certificate business. For its Charge Card products, TRS uses interest rate swaps to achieve a targeted mix of

fixed and floating rate funding. These interest rate swaps are used to protect the company from the interest rate risk that arises

from short-term funding. AEFA uses interest rate products to hedge the risk of rising interest rates on investment certificates which

reset at shorter intervals than the average maturity of the investment portfolio.

At December 31, 2001, the company expects to reclassify $208 million of net pretax losses on derivative instruments from

accumulated other comprehensive income (loss) to earnings during the next twelve months. These losses will be recognized in

earnings during the terms of those derivatives contracts at the same time that the company realizes the benefits of lower market

rates of interest on its funding of Charge Card and fixed rate lending products.

Currently, the longest period of time over which the company is hedging exposure to the variability in future cash flows is 5 years

and relates to funding of foreign currency denominated receivables.

FAIR VALUE HEDGES

The company uses derivatives to hedge against the change in fair value of some of its investments in public companies. Changes

in the fair value of the derivatives are recorded in earnings along with related designated changes in the spot price of the underly-

ing shares. Changes in the time value elements of these derivatives are considered as hedge ineffectiveness.

The company also uses interest rate swaps to hedge its firm commitments to transfer, at a fixed rate, receivables to trusts estab-

lished in connection with its asset securitizations. AEFA is exposed to interest rate risk associated with its fixed rate corporate bond

investments. AEFA enters into interest rate swaps to hedge the risk of changing interest rates as investment certificates reset at

shorter intervals than the average maturity of the investment portfolio.

During 2001, the company recognized a pretax net loss of $1.2 million primarily related to the time value element of its fair value

hedging instruments. This amount is included in other expenses in the Consolidated Statements of Income.