American Express 2005 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2005 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

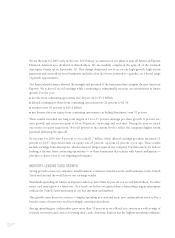

$1.00

$1.61

$1.80

$2.09

$2.56

01 02 03 04 05

$3.0

$2.5

$2.0

$1.5

$1.0

$0.5

$0

bers of any card network, and our continuing efforts to deepen relationships with these customers helped us

to expand our lead in 2005.

We also added 5.6 million new cards-in-force during the year, one of our largest annual increases ever. This

brought total cards-in-force to 71 million, a 9 percent increase from a year ago. In growing our cardmember

base, we continued to target the kind of high-spending cardmembers who are synonymous with the

American Express franchise.

While spending is the focus of our business model, lending is an important complement. We had outstand-

ing growth in cardmember loans, which rose 15 percent on a managed basis and 23 percent on a GAAP basis

in 2005. This performance compared favorably to our competitors, most of whom posted only single-digit

gains in managed loans.

As we have grown cardmember spending and lending balances at a rapid pace, we have also maintained strong

credit quality. Write-off rates in both our charge and lending portfolios remained near all-time lows, despite

an industry-wide spike in bankruptcy filings in the second half of the year that stemmed from new federal

legislation in the United States. The impact was well controlled, and we expect the new laws will have a

slightly beneficial effect over the long term.

Overall, the results from our card business in 2005 showed the competitive advantages of our spend-centric

model, the benefits of our business-building investments over the past few years, and our emphasis on

providing superior value to our cardmembers and merchant partners.

A STRONGER, MORE FOCUSED COMPETITOR

Our momentum is strong, and we believe it will be further fueled by our spin-off of Ameriprise. The spin-off

was a major change for American Express, but it was also part of a logical evolution for our company. Enter-

ing 2005, our proprietary card-issuing business was in an excellent competitive position following several

years of rapid growth. In addition, the opening of our network services business in the United States created

new opportunities for us.

In view of the high returns and broad range of growth opportunities across our payments businesses, we con-

cluded that sharpening our focus on these activities would accelerate our growth. Likewise, we believed

Ameriprise would benefit from operating as an independent company. The spin-off gave shareholders an

interest in two outstanding companies, each pursuing its most important priorities and objectives.

AXP / AR.2005

[ 11 ]

DILUTED EARNINGS PER SHARE FROM CONTINUING OPERATIONS

In 2005, diluted earnings per share from continuing operations rose 22 percent, driven by

higher cardmember spending and a continuing focus on containing costs.