American Express 2005 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2005 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

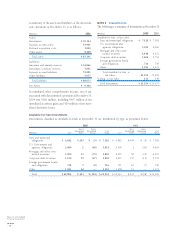

lending. Securitization transaction costs are offset

against the gains on sales at the time of the transaction.

During 2005, 2004 and 2003, the Company sold

$5.4 billion, $3.9 billion and $3.5 billion, respectively,

of cardmember loans, or $5.4 billion, $3.9 billion and

$3.1 billion, respectively, net of the Company’s invest-

ments in subordinated retained interests. Additionally,

during 2005, 2004 and 2003, $4.5 billion, $3.0 billion

and $1.0 billion, respectively, of securities issued to

investors from the Lending Trust matured. The pretax

net gains on sale from securitizations, including the sale

of subordinated retained interests, net of the impact of

maturities, the effect of changes in interest-only strip

valuation factors and a reconciliation adjustment charge

were $21 million, $26 million and $124 million, respec-

tively, for 2005, 2004 and 2003.

Management utilizes certain estimates and assumptions

to determine the fair value of the subordinated retained

interests, including the interest-only strip. These esti-

mates and assumptions are generally based on projec-

tions of finance charges and fees paid related to the secu-

ritized assets, net credit losses, average loan life, the

contractual fee to service the transferred assets and a dis-

count rate commensurate with the retained interest.

Changes in the estimates and assumptions used may

have a significant impact in the Company’s fair valua-

tion. The key economic assumptions used in measuring

the subordinated retained interests at the time of issu-

ance and during 2005 and 2004 were as follows (rates

are per annum):

2005 2004

Weighted average loan

life (months) 44

Expected credit losses 3.30%–3.90% 3.98%–4.67%

Subordinated certificates

discounted at 2.6%–4.8% 1.2%–3.5%

Residual cash flows

discounted at 12.0% 8.3%–12.0%

Returns to investors

Variable

Fixed

Contractual

spread

over LIBOR

ranging from

.00% to .90%

1.7%–5.8%

Contractual

spread

over LIBOR

ranging from

.04% to .90%

1.7%–7.4%

The following table presents quantitative information

about delinquencies, net credit losses and components

of securitized cardmember loans on a trust basis at

December 31:

(Billions)

Total

Principal

Amount

of Loans

Principal

Amount of

Loans 30

Days or

More Past

Due

Net

Credit

Losses

During

the Year

2005

Cardmember loans managed $ 54.3 $ 1.3 $ 2.1

Less: Securitized

cardmember loans sold 21.2 0.6 1.0

Cardmember loans on

balance sheet $ 33.1 $ 0.7 $ 1.1

2004

Cardmember loans managed $ 47.2 $ 1.2 $ 2.0

Less: Securitized

cardmember loans sold 20.3 0.6 1.0

Cardmember loans on

balance sheet $ 26.9 $ 0.6 $ 1.0

The key economic assumptions and the sensitivity of the

current year’s fair value of the interest-only strip to

immediate 10 percent and 20 percent adverse changes

in assumed economics are as follows:

(Millions, except rates per annum)

Monthly

Payment

Rate

Expected

Credit

Losses

Cash Flows from

Interest-only

Strips

Discounted at

Assumption 26.2% 3.5% 12.0%

Impact on fair value of

10% adverse change $ 13 $ 17 $ 0.4

Impact on fair value of

20% adverse change $ 26 $ 34 $ 0.8

These sensitivities are hypothetical and will be different

from what actually occurs in the future. Any change in

fair value based on a 10 percent variation in assumptions

cannot be extrapolated in part because the relationship

of the change in an assumption on the fair value of the

retained interest is calculated independent from any

change in another assumption; in reality, changes in one

factor may result in changes in another, which magnify

or offset the sensitivities.

Notes to Consolidated

Financial Statements

AXP / AR.2005

[78 ]